September 2024 Portfolio Update

September 2024 Portfolio Update

Including all current investment ideas.

Irrational Analysis is heavily invested in the semiconductor industry.

Please check the ‘about’ page for a list of active positions.

Positions will change over time and are regularly updated.

Opinions are authors own and do not represent past, present, and/or future employers.

All content published on this newsletter is based on public information and independent research conducted since 2011.

This newsletter is not financial advice, and readers should always do their own research before investing in any security.

Feel free to contact me via email at: irrational_analysis@proton.me

Hello wonderful subscribers. A lot of you are new, thanks to Asianometry Jon’s recent recommendation. (for which I am eternally grateful for)

Want to take this opportunity to disclose all my holdings and give quick updates on what I am actively buying and general investment opinions.

Have some really exciting technical material in-progress but unfortunately, I am quite busy with my dayjob.

Quality content will have to wait. Here is some low-quality stuff in the meantime.

Contents:

Portfolio Overview

Top 3 Largest Accounts YTD Performance

What I am presently buying, shorting, and trading. (no particular order)

Keysight

Fabrinet

Ciena

Long Broadcom/TSMC/ARM, Short Qualcomm

Abbvie

GE Vernova

First Solar

Ideas I am not participating in but want to write about anyway.

Intel Short

AMD ???

Eli Lilly

Astera Labs Short

Wildcard: Verizon

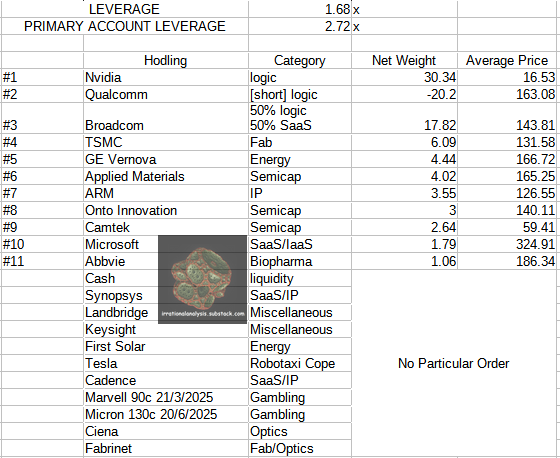

[1] Portfolio Overview

Every penny I have (excluding 401K which is mutual funds) is accounted for.

My primary account is Webull because I love the mobile UI. All the leverage is in that account. Need the ability to quickly assess and add/cut risk on my phone while at work within 90 seconds in-between meetings.

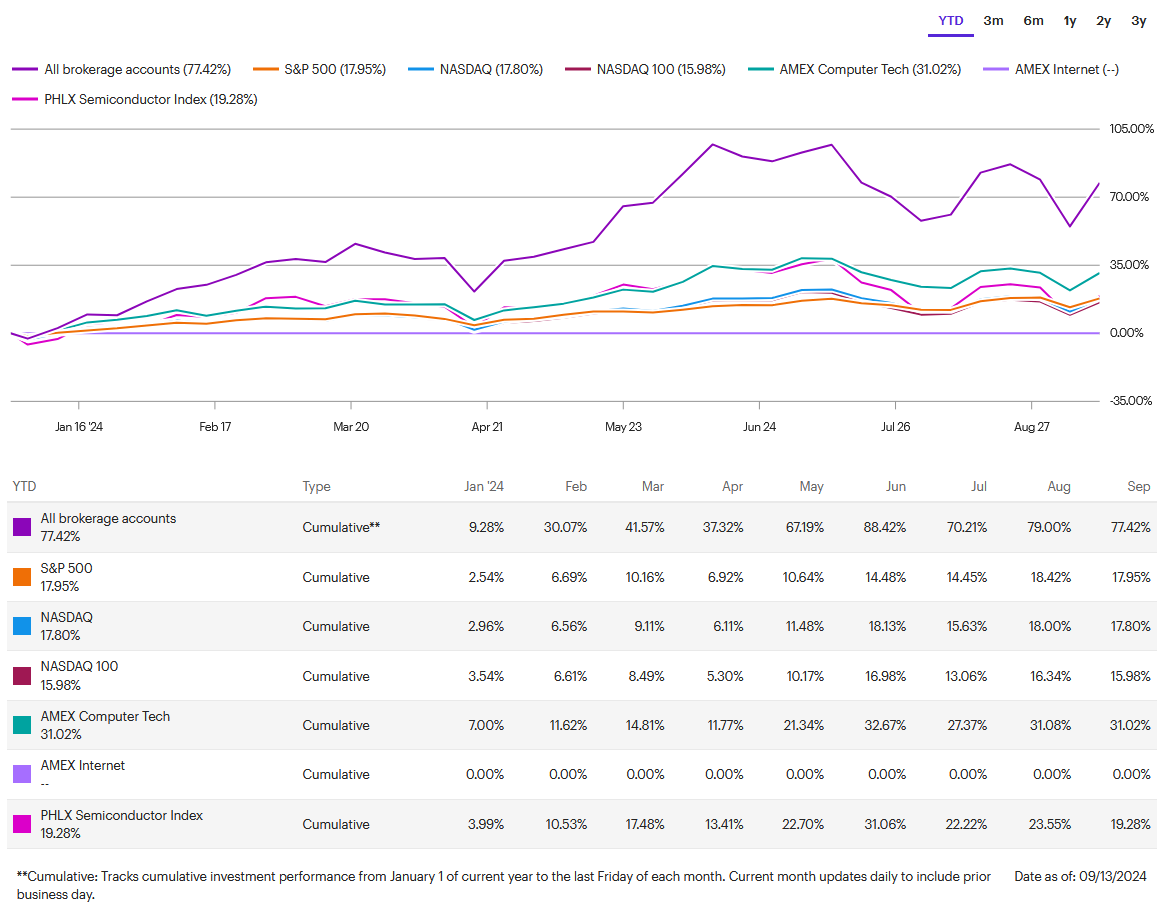

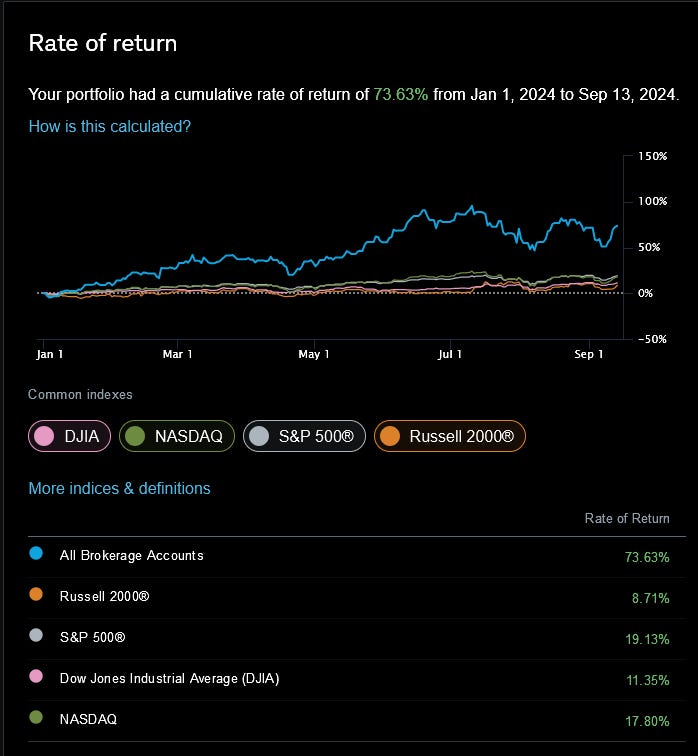

[2] Top 3 Largest Accounts YTD Performance

Webull:

My personal goal is for this account to outperform SMH 0.00%↑ (market-cap weighted semiconductor ETF) by at least 30% by the end of this year.

Made several really stupid mistakes this year that killed a lot of profits. Plan to make the most of the last 3.5 months of this year.

This is a multi-strategy account:

Long/Short

Unhinged OTM Options Gambling

LEAP

Earnings Weeklies YOLO

Writing covered calls at the bottom and immediately losing huge quantities of money.

ETRADE:

These accounts are long-only. Occasionally write covered NVDA 0.00%↑ calls and actually made decent money this year with this strategy.

Schwab:

Again, long-only. Zero trading. These accounts are the most diversified from a sector perspective.

[3] What I am presently buying, shorting, and trading. (no particular order)

My opinions and behaviors change daily based on market behavior. Don’t take the ordering of this section too seriously.

[3.a] Keysight

Nothing to add. Clicky the linkey.

[3.b] Fabrinet

I am very bullish optics after reading this SemiAnalysis piece.

Fabrinet basically is a worse version of TSMC (much lower margins) that only does optics. I previously held FN 0.00%↑, got pissed at their deceitful management, and 100% liquidated at a modest profit.

![[Q1 CY24] ARM Short Squeeze, Fabrinet Sus](https://substackcdn.com/image/fetch/w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F75bed919-502d-4786-bb23-79f4ed882183_889x886.png)

I have bought back in, despite the sus management.

Low-risk, medium reward optics play. Will explain in more detail in the upcoming communication systems post.

[3.c] Ciena

Similar to above. Optics play because of the SemiAnalysis multi-datacenter training piece.

High-risk, high reward optics play. Will explain in more detail in the upcoming communication systems post.

[3.d] Long Broadcom/TSMC/ARM, Short Qualcomm

This is a large spread trade I am running. Debate me in the comments section or via private email if you disagree. We shall have such fun.

Here is a quick summary of the catalysts for this trade.

Positive:

ARM:

Massive datacenter exposure that sell-side has not correctly accounted for.

Will get a boost from v9 royalty rate hikes on Apple and MediaTek.

I beleive that ARM is going to win the Qualcomm/Nuvia lawsuit and force a settelemnt with a much higher royalty rate. Sell-side cannot model this outcome for either ARM 0.00%↑ or QCOM 0.00%↑.

Broadcom

Will get large incremental RFFE content with Apple in 2025 as the Apple modem rolls-out.

Incredible upside potential from semi-custom AI ASICs that has been conservatively guided by sell-side.

Co-packaged optics solution is incredible. A Q4 2025 volume ramp is genuinely possible. 100% confident in H2 2026 ramp.

The suffering of VMWare customers who are locked-in is our (shareholder) gain.

Regular semiconductor portfolio (excluding DOCSIS) has mostly bottomed.

TSMC

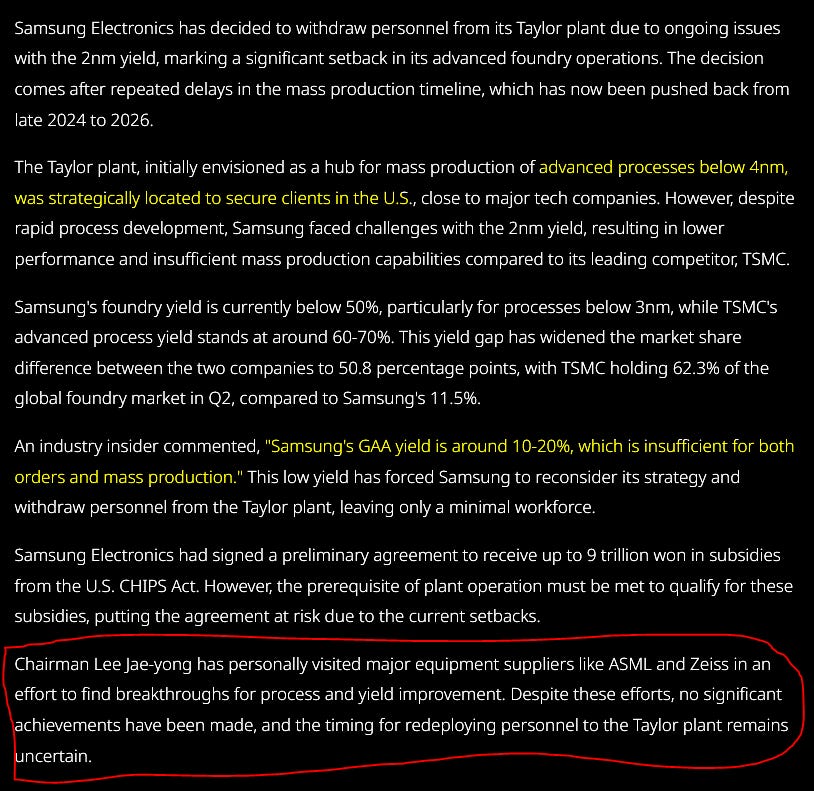

Samsung foundry is catastrophically failing on their 3nm-class nodes that perform worse than TSMC N5 (yes original N5) and yield at sub-20% for tiny smartphone SoCs (should be 70%).

Intel is dealing with serious issues which I will write about soon.

Source: If you repeatedly smash your thumb with a hammer, can the hammer (tool) manufacturer help you use the tool correctly?

Qualcomm

Qualcomm’s iPhone modem share will decay from 100% in 2024 to 60%/20%/0% in 2025/2026/2027. (I am much more bearish than sell-side)

Investors will be disappointed in AI PC sales guidance on the upcoming November 19 Investor Day.

Continued share losses to MediaTek and Apple.

Modest share losses to the Xiaomi internally developed apps processor paired with a Unisoc 5G thin modem.

Inability to pass-on TSMC N5 and N3 price hikes onto customers, leading to QCT gross-margin degradation.

China macro seems bad, so handset sales growth may disappoint due to lengthening replacement cycles from low consumer confiddence.

Negative

ARM:

The new Qualcomm chips (Q1 2025 volume shipments) will use the internal Nuvia cores which are also V8. (double hit from v9 TLA to v8 ALA)

Lawsuit may drag out, temporarily benefiting Qualcomm’s gross margins and harming ARM’s royalty revenue until a lump-sum payment hits.

Qualcomm

Automotive revenue may (probably will) continue to out-grow sell-sides expectations.

Automotive guidance from the November 19 Investor Day may offset lackluster AI PC guidance.

Apple’s modem might fail carrier qualification within certain regions at the last minute, providing temporary upside in 2025.

[3.e] Abbvie

I have done some surface-level research into biopharma majors and settled on ABBV 0.00%↑ for now. Thier products are for treating really nasty, chronic conditions. Strong pricing power and lifelong users.

Thier R&D efforts seem pretty good. Divided and P/E are solid.

[3.f] GE Vernova

This company is marketed as a clean energy (wind turbine) play. They are not.

GEV 0.00%↑ makes the vast majority of its money from natural gas turbines. They also have exposure to electrical grid transformers. Both of these will be critical in the coming wave of USA energy grid capacity buildout for AI infrastructure.

I will not invest in oil or coal because of ethical reasons. But natural gas… is fine. We need a base-load power source on the grid and many governments have stupidly shunned nuclear.

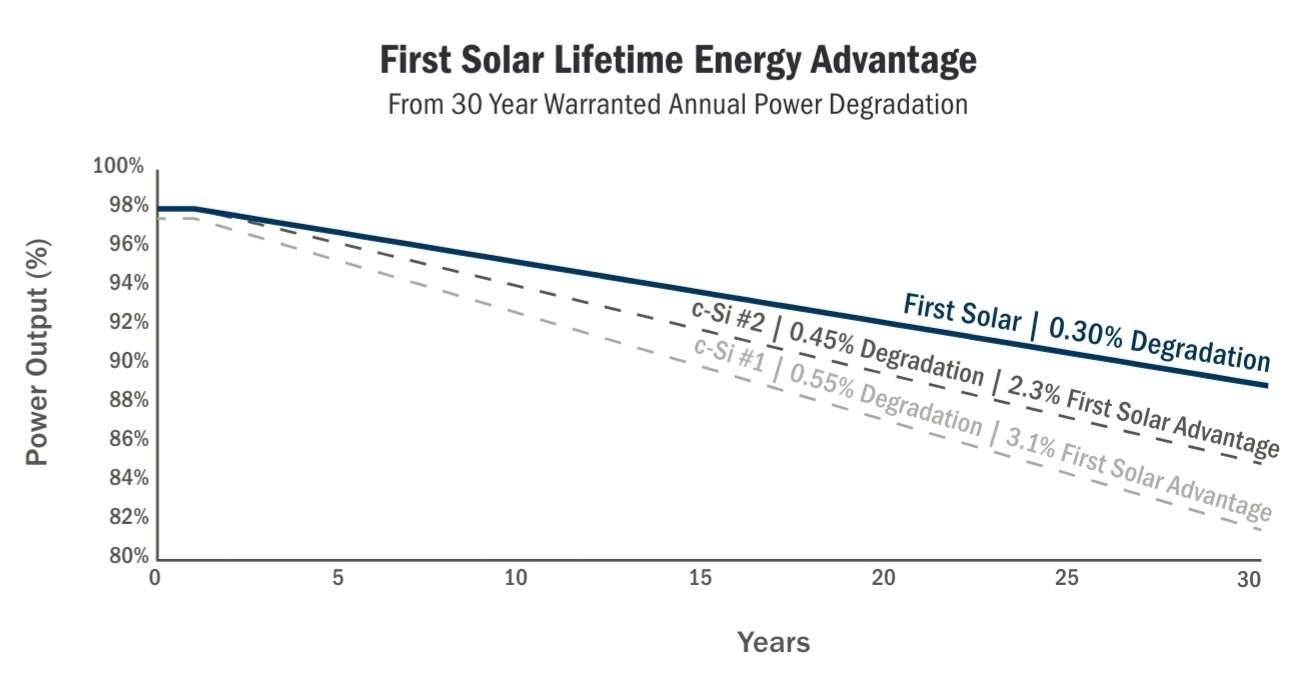

[3.g] First Solar

Solar panels degrade over time. The above plot is from a FSLR 0.00%↑ datasheet and is literally my entire investment thesis.

They claim to have superior engineering that leads to much more economical solar panels in a large-scale grid environment (not the residential stuff).

Problem is that this stock depends on government policy, the worst kind of dependency.

Tariffs against Chinese solar panel dumping.

Clean energy subsidies, tax incentives, and other governmental assistance.

[4] Ideas I am not participating in but want to write about anyway.

Reasons for not participating:

Ethical conflicts.

Risk is too high.

Don’t understand the space well enough.

A combination of the above.

[4.a] Intel Short

I genuinely believe there is a 30% chance INTC 0.00%↑ goes bankrupt in the next 18-24 months.

![[2Q2024] $AVGO $NVDA $MRVL + $INTC Chaos Update](https://substackcdn.com/image/fetch/w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F6dd98ab1-cb86-4b0f-89c5-f70e30d2f3d9_848x484.png)

I agree with Stacy. Shorting Intel is not worth it. Just avoid it. Radioactive garbage should be avoided. It’s not a plaything.

I strongly disagree with the modeling done by Bernsein Research and BoA. Gross margin and revenue assumptions are completely wrong.

There is a huge gap between what the financial community thinks will happen to Intel in the short term and what is actually going to happen. Problem is… the stock can jump 20% in one day on hopium news like Altera spinout.

Maybe US Commerce Secretary Raimondo should ask INTC 0.00%↑ shareholders to use Intel Foundry for AI chips, instead of wasting the time of Nvidia shareholders.

Intel Gaudi 1, Gaudi 2, Gaudi 3, and Falcon Shores are all 100% fabbed by TSMC.

STOP BEGGING FOR GOVERMENT HANDOUTS AND FIX THE PDK.

YOUR OWN INTERNAL AI CHIP DESIGN TEAMS REFUSE TO USE INTEL 3 AND INTEL 18A.

COMPLAINING TO THE COMMERCE DEPARTMENT WONT FIX ANYTHING.

[4.b] AMD ???

I have literally no idea if AMD 0.00%↑ is a long or a short.

Strongly believe MI300/325X sales will tank in Q1 once Blackwell ramps. Sell-side has modeled growth of AMD DC GPU… wrong!!!

But there was a Su Bae comment that caught my attention at a recent investment bank (GS) conference.

She basically said something along the lines of…

“We want to work well with the hyperscale’s, including semi-custom solutions.”

Facts:

AMD has an excellent semi-custom silicon team that has worked with MSFT 0.00%↑ and Sony on video game console custom chips.

The relationship with MSFT 0.00%↑ is excellent from many generations of partnership on the XBOX SoC.

AMD has excellent PCIe, memory PHY, and CPU IP.

AMD (with the addition of Xilinx) is the industry pioneer of advanced packaging, chiplets, hybrid-bonding, and 3D-IC.

FPGA IP from Xilinx could be useful in niche inference cases.

I think there is a real chance Microsoft moves Maia over to AMD semi-custom. Or at least, AMD gets a semi-custom win within the next year or two.

Shorting AMD is not worth it IMO. Might buy some puts in November for fun.

[4.c]

I still think ALAB 0.00%↑ is comically overvalued. The sell-side notes I have read on this ticker are hilariously uninformed and way waaaaay too bullish.

Search my substack for more prior commentary on ALAB. PCIe switch sales to Amazon (who has market-distorting warrants incentivizing purchases) won’t save them from the impending revenue implosion from no re-timers in GB200.

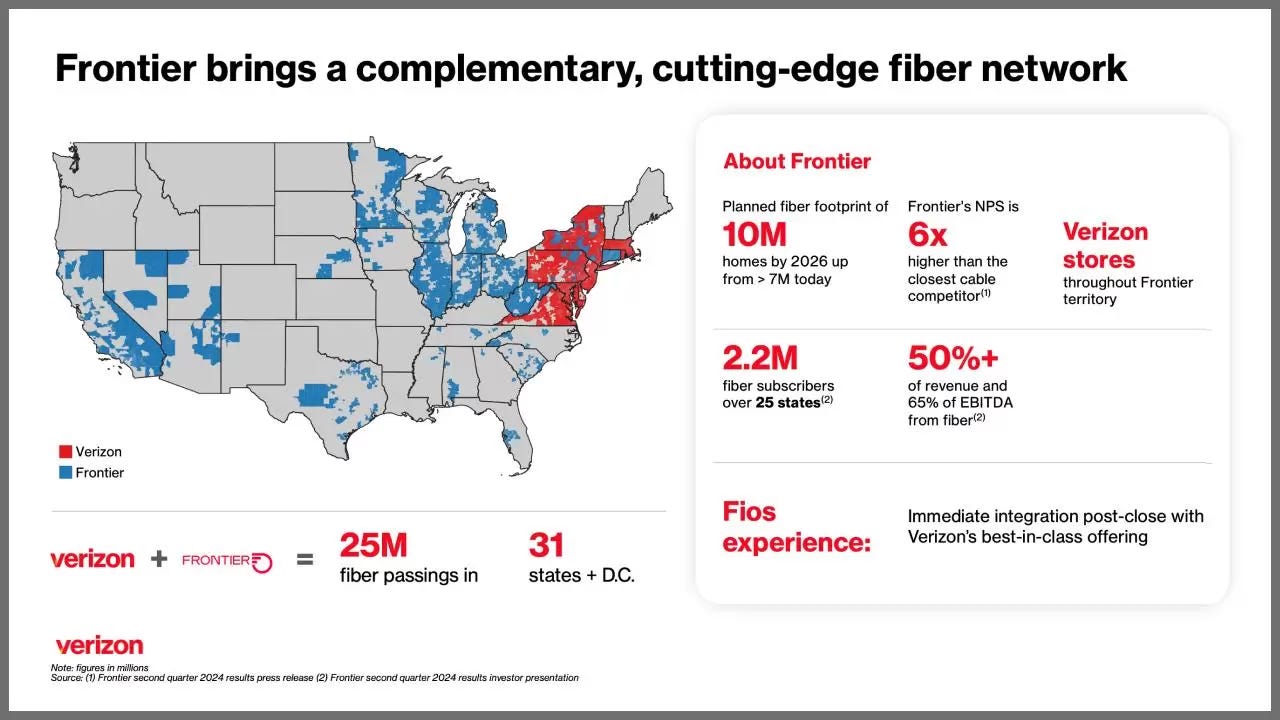

[4.d] Wildcard: Verizon

Verizon recently bought back a lot of fiber that they previously spun out. This acquisition is very suspicious. The plan they have publicly stated is they want to bundle fiber home internet with wireless/cellular plans.

I have a conspiratorial theory that VZ 0.00%↑ bought Frontier to lease fiber lines to hyperscalers for multi-datacenter AI training.

Look at the map… Texas and Midwest…

High-risk, high reward optics play. Will explain in more detail in the upcoming communication systems post.

I’m more concerned about AVGO VMWare customer loss, don’t you think if sufficiently pissed customers will take the opportunity to begin working towards alternatives? Been reading that competitors have seen substantially increased interest/sales in the wake of the acquisition