Astera Labs: Impending Revenue Implosion in Plain Sight

Attractive trading opportunity.

IMPORTANT:

Irrational Analysis is heavily invested in the semiconductor industry.

Please check the ‘about’ page for a list of active positions.

Positions will change over time and are regularly updated.

Opinions are authors own and do not represent past, present, and/or future employers.

All content published on this newsletter is based on public information and independent research conducted since 2011.

This newsletter is not financial advice and readers should always do their own research before investing in any security.

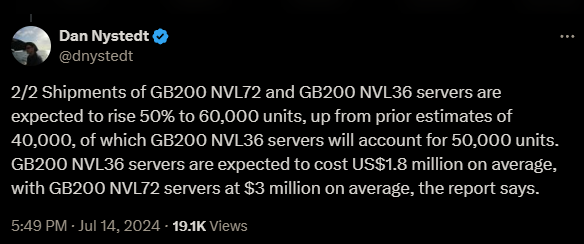

A brief note on ALAB 0.00%↑ because several people have pinged me on this name in the last month or so.

Astera Lab’s revenue is about to implode. This information is public and in plain sight, but many seem to have missed it.

![[GB200 NVL72] The Mainframe of Doom](https://substackcdn.com/image/fetch/$s_!_hFr!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F9b4c8e16-a994-40a1-a08d-07d4a9448536_647x846.png)

I previously made the call that GB200 NVL72/36 integrated mainframes would have massive traction and share of the Blackwell platform right after GTC. This was the right call based on engineering-driven investment analysis.

This is good for ARM 0.00%↑ which I highlighted in this post back when ARM was trading at < $120/share.

Sidenote: I was not expecting ARM to rise ~50% in less than two months. This is an absolutely crazy valuation. Holding on to my 0.6% weight position but be careful investing into ARM at the current price of $178/share. Softbank secondary offering has to be incoming.

Anyway… what does this have to do with Astera Labs?

Facts:

The vast majority of ALAB revenue is from PCIe re-timer chips. (> 95%)

By far, the two largest customers are NVDA 0.00%↑ and AMZN 0.00%↑

Amazon has purchase-volume based warrants which incentivizes them to single-source.

Nvidia does not want to prop up AI semi-custom ASIC vendors such as AVGO 0.00%↑ and MRVL 0.00%↑ so there is a strong incentive to continue single-sourcing.

ALAB has ZERO CONTENT in GB200 NVL systems.

Re-timers extend reach and help with loss (how long the channel is) and reflections (how many connectors, medium changes, …) there are. A short, simple channel that only passes through a single PCB (no backplane, no extra connectors/cables) does not need re-timing.

Astera Lab’s revenue from their largest customer is about to get cut in half. The evidence is in plain sight.

This ticker is an attractive short candidate. Unfortunately, I cannot participate because of ethical reasons.

Normal analysts rate stocks with terms like “Outperform”, “Market Perform”, and so on.

My rating for ALAB 0.00%↑ is “imminent violent sinusoid”.

No idea what the amplitude or frequency of the sinusoid will be, but this ticker is definitely going way down because of Grace-Blackwell then will recover later because of Trainium/Inferentia.

Good luck, have fun.

I like the trade. I would highlight a few risks though:

1) float's only 21.7M shares, ~14% of the 155.7M shares outstanding

2) short interest is 7.9M shares, ~36% of the float, as of June 28 (don't have more recent data)

could be quite volatile until the lockup expiry of Sept 16, esp if this small cap mean reversion rally continues

Great read, short and to the point. Thanks, I appreciate all your insights.