[2Q2024] $AVGO $NVDA $MRVL + $INTC Chaos Update

Resignations! Emergency Board Meetings! Canceled Fabs!

IMPORTANT:

Irrational Analysis is heavily invested in the semiconductor industry.

Please check the ‘about’ page for a list of active positions.

Positions will change over time and are regularly updated.

Opinions are authors own and do not represent past, present, and/or future employers.

All content published on this newsletter is based on public information and independent research conducted since 2011.

This newsletter is not financial advice, and readers should always do their own research before investing in any security.

Feel free to contact me via email at: irrational_analysis@proton.me

Broadcom:

I have a large, levered up long position that got crushed today.

The numbers were rather disappointing. Google seems to not be ordering as many TPUs as buy-side was hoping for.

Enterprise has been decisively called as a bottom which is great news. Broadband (DOCSIS) still imploding but whatever. DOCSIS was the one business I completely wrote-off when developing my AVGO 0.00%↑ investment thesis.\

Positive foreshadowing. I may be in copium mode.

Very bullish on the super-chiplet platform. I may be 2-3 quarters early but I’m not wrong. Just need to stay solvent in the meantime.

Seems like infrastructure (datacenter cooling and power) is causing a temporary slowdown. A holding pattern.

Nvidia:

The psychological turmoil leading up to NVDA 0.00%↑ print was hilarious.

They had to change some upper metal layers to spread out bump-out and enable higher yields on CoWoS-L packaging. Everything we knew about and suspected was confirmed. Fears of a wider delay were not based in engineering reality.

Great job to every TSMC and Nvidia engineer who pulled this emergency fix off. The global economy thanks you for your several months of suffering.

Multiple sell-siders asked bad questions that allowed Mr. Leather Jacket to spout useless speeches. Stacy Rasgon (Bernstien) finally asked an intelligent question.

Gross-margin dilution features are overblown. Nvidia CFO was more explicate in buy-side callbacks. She said that Q4 is the bottom for gross-margin. Very good news.

He seems salty lol.

Overall everything is fine. I was quite concerned that AVGO 0.00%↑ custom silicon would add pricing (ASP) pressure on Nvidia and thus dilute gross-margins to 70-72%.

NVDA 0.00%↑ remains my largest position. I sold some covered calls (which became instantly worthless after the earnings report) to hedge. Spent that cash on other names.

I continue to believe that Nvidia will hit at least $150/share sometime in H2 next year. That is when I start selling to diversify.

Nothing has changed. Have faith in superior engineering.

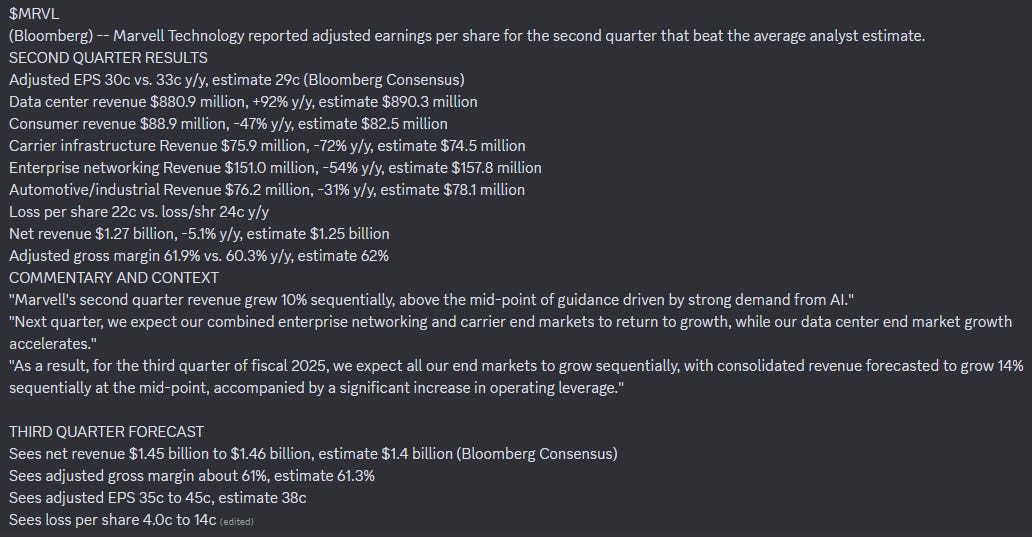

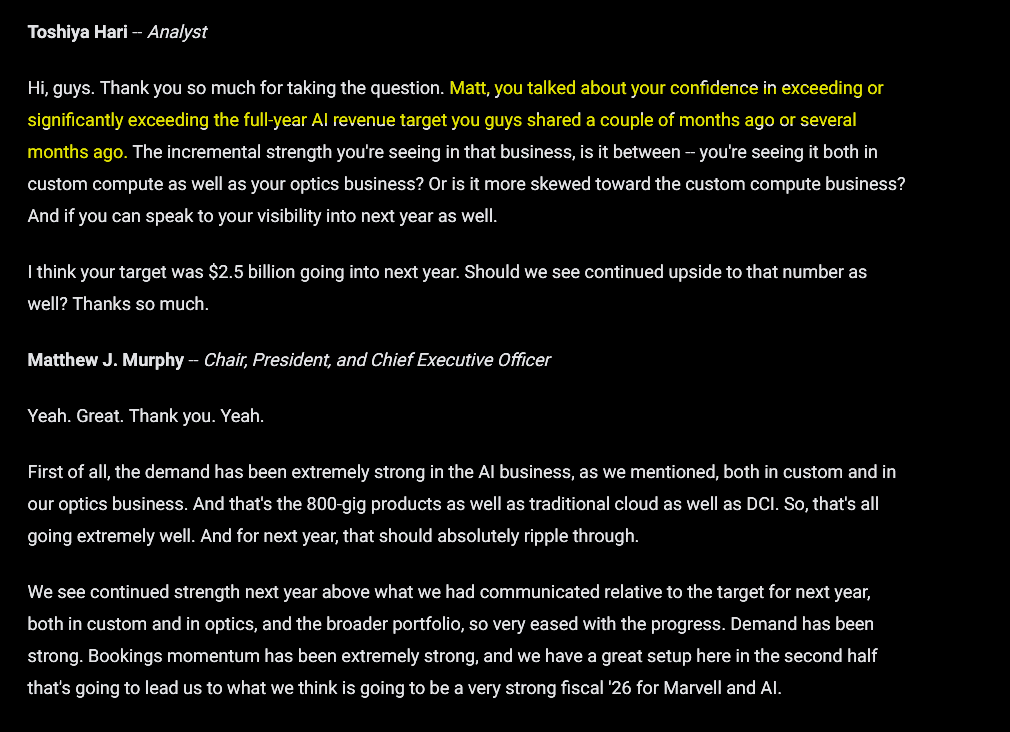

Marvell:

Custom silicon ramp is happening but not fully materialized yet. More upside incoming. The oDSP and electrical DSP business is gona continue going parabolic.

Nobody cares about CXL. The MRVL 0.00%↑ Ethernet switches are not competitive. Only Amazon has cheeped out to use them. Broadcom and Nvidia switching much better.

The bottom is finally in.

Marvell’s telco-focused DPUs are very good. Margins on the 5nm new products should be much better. We don’t just have a bottom forecast… we are past the bottom.

Everyone knew they were sandbagging the Amazon ramp. Buy-side thesis was largely built around this.

Analyst: Can you please provide clarity on the Amazon ramp?

Managment: haha no (◕‿◕✿)

I have a small options position (90c, March 2025) and have no intention to add or close out. Amazon ramp has not hit yet. When that frenzy happens, gamboling position goes to the moon. That is the hope at least.

Intel Special Update:

What the hell is going on at INTC 0.00%↑?

Let’s start with the event that kicked all this mayhem.

Lip-Bu Tan essentially resigned in protest. This is really bad.

What is worse is a separate Reuters report only a week later that Broadcom saw unacceptable yield on their 18A test wafers.

Defect density (D0) is a common metric in semiconductor manufacturing. It represents the number of defects expected per unit area, typically centimeters squared (cm^2).

D0 is highly guarded.

This number is the most top-secret shit in this industry.

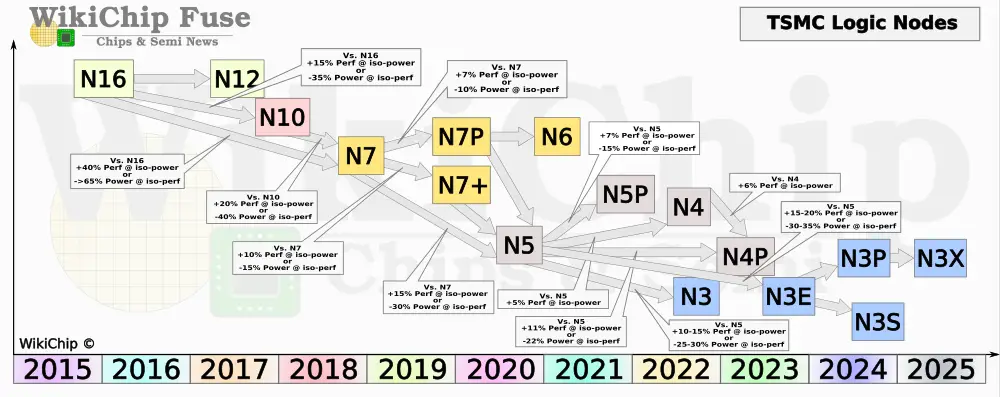

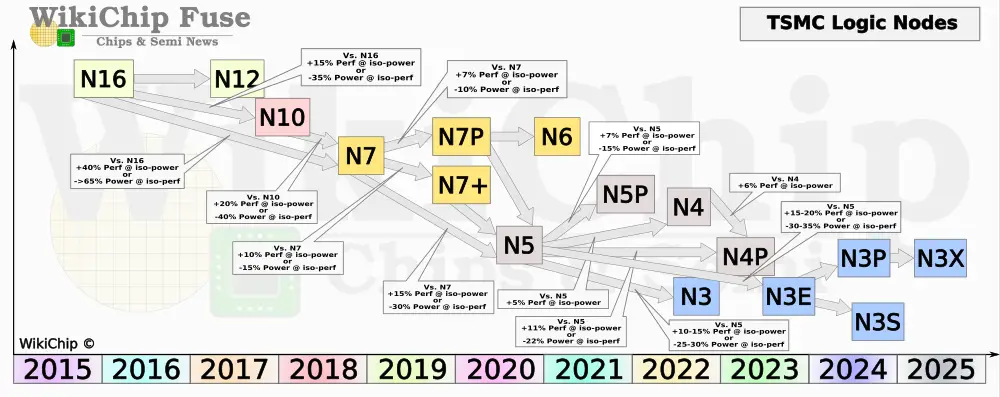

TSMC has previously published their D0 for N10, N7, and N5 because it was very good. They have since stopped publishing for new nodes. There is no public D0 data for N3B (did not go well) or N3E/P (redo, much better).

Typically, you want D0 to be at around 0.1 for high-volume manufacturing. A D0 of 0.35 to 0.5 is expected at 3-4 quarters before high-volume ramp.

The Reuters reporter (Max Cherney) should not have three sources on Broadcom’s failed 18A evaluation. Such extraordinarily sensitive information related to D0 should not be with the press! Yield on these Broadcom test wafers must be horrific. These “three sources familiar with the matter” must be livid.

As is standard practice in journalism, Reuters requested comment from both Intel and Broadcom. Both companies also knew when the story would go live.

On the same day as the Reuters Broadcom 18A story (September 4th, 2024), Intel put out this blog post.

20A is canceled. They are moving all planned Intel Products chiplets from 20A to TSMC N3! Intel’s claim that 18A D0 is less than 0.4 almost certainly refers to their internal products D0. If 18A D0 was actually that good for third parties, Broadcom people would not be airing top secret dirty laundry to the press!

Canceling 20A is actually a really bad sign. Intel 18A is a derivative node of 20A, similar to how TSMC N4 and N4P are derivative nodes of N5.

{kind=link}

Here is how derivative nodes work:

Low single-digit lithography mask shrink.

Updated (slightly better) standard cells and libraries.

Minor improvements in expected process skew.

A combination of all of the above.

TSMC N7 and N7P and N6 are not fundamentally different.

Same for TSMC N5, N5P, N4, and N4P.

The performance/power gains from derivative nodes are heavily dependent on the design, often not as good as advertised by the foundries. This is true for every foundry.

Intel’s claim that they are canceling 20A because “18A is so good” is nonsensical.

A much more logical explication is 18A is not going well for 3rd party customers such as Broadcom and they are surging engineers to fix it.

This does not pass the smell test.

Unfortunately, I smell a dumpster fire.

Planning to share my updated portfolio weights and average prices for all > 5% positions soon. Spreadsheets are not my strong suit.

Recent market chaos is lots of fun.

Actively buying FN 0.00%↑ KEYS 0.00%↑ ARM 0.00%↑ and TSM 0.00%↑.

Have a large leveraged spread trade in my main account. Long AVGO 0.00%↑ TSM 0.00%↑ ARM 0.00%↑ , short QCOM 0.00%↑.

AMD 0.00%↑ might be a good short in the near future.

INTC 0.00%↑ is a do-not-touch. The equity is radioactive garbage. Owning radioactive garbage is a bad idea. Borrowing radioactive garbage and short selling it to someone else is also a bad idea.

It’s just money. It’s made up.

I have abt 10% of my portfolio in Qualcomm so I'm really interested in why you are shorting it, especially since you are going long on ARM

If you’re shorting QCOM just for Apple modem, hasn’t Qualcomm provided long term earnings growth guidance assuming zero Apple revenue? It seems like Apple modem loss is already baked in.