2026 Irrational Ideas

Obscure and Dangerous Only!

Irrational Analysis is heavily invested in the semiconductor industry.

Positions will change over time and are regularly updated.

Opinions are authors own and do not represent past, present, and/or future employers.

All content published on this newsletter is based on public information and independent research conducted since 2011.

This newsletter is not financial advice, and readers should always do their own research before investing in any security.

Feel free to contact me via email at: irrational_analysis@proton.me

Welcome to the second edition of Irrational Ideas, a list of dangerous and obscure investment ideas that intentionally avoids obvious stuff.

So no Nvidia or Broadcom or TSMC.

Also none of the semicap majors. Yes, Lam Research is gona do well because of memory capex cycle. This is obvious and boring.

New to this year is a “top pick” column that highlights the most retarded ideas for illiterate morons with less attention span than a zoomer brain-damaged by TikTok and GPT 4o sycophantic glazing.

Also, this year there are many more names to cover so I will write about the following high-level sections:

Optics/Connectivity

Semicap

Energy

Timing

Logic Fab

Miscellaneous Longs

Funding and Tactical Shorts

Dogshit (Neoclouds)

Marvell (they get their own category lmao)

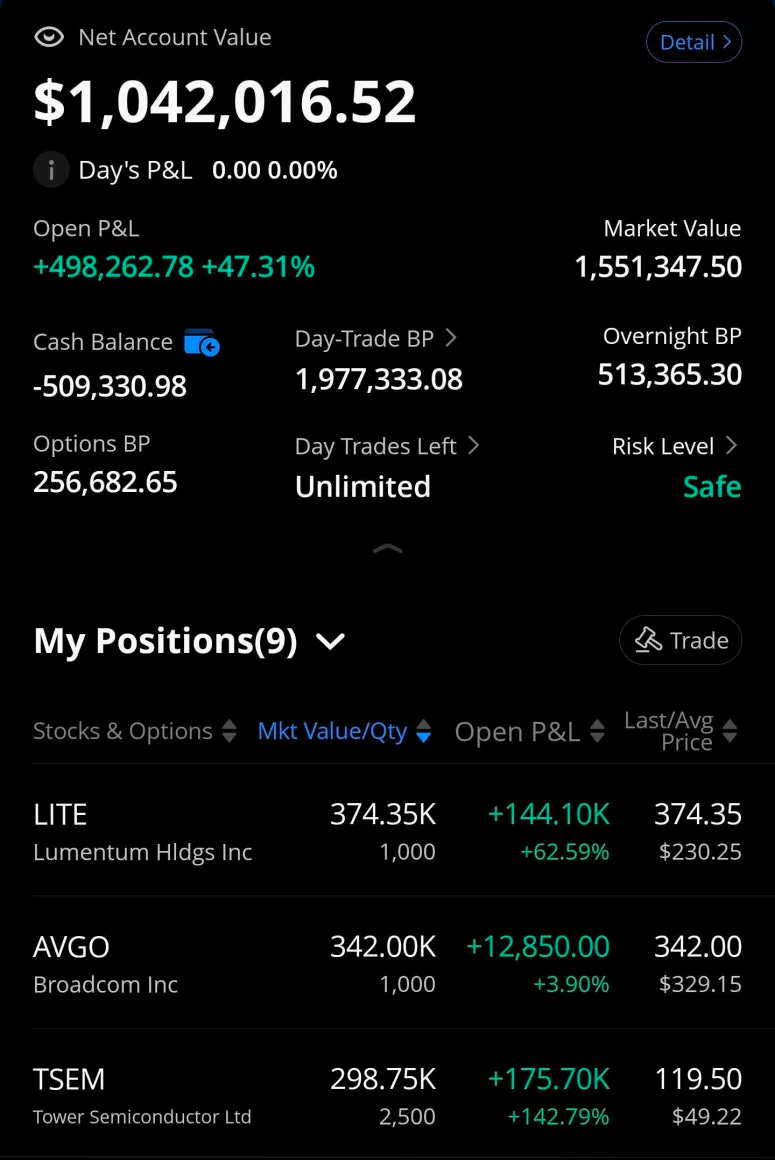

Note: Full portfolio update (trading and long-only) alongside all trading account statements and CSV of trading records will be published on the last trading day of 2025. (December 31st after market close). For now, a brief update of trading account at the time of writing.

[1] Optics/Connectivity

Almost everything in this category is going to the moon but some will win more than others.

My top picks in this section are for the following reasons:

Lumentum ( LITE 0.00%↑ )

Monopoly on ultra-high-power, narrow-linewidth lasers for CPO applications.

Highest quality EML in the world.

OCS is upside others believe in but I don’t…

Tower Semi ( TSEM 0.00%↑ )

Effective monopoly in silicon photonics fab market.

GloFo sucks. (more on this later)

Price/Book is still well under TSMC and kinda reasonable.

SiPho has much better margins than the RF junk Tower sells.

Some minor torque to Apple modem via Qorvo envelop tracker.

VCSEL is dead at 200G/lane, EML is critical shortage, LONG LIVE SIPHO 1.6T TRANCEIVER.

Ciena ( CIEN 0.00%↑ )

Excellent in-house 400G SerDes.

Excellent packaging and cooling innovations.

Massive wave of WDM equipment upgrades coming for DCI buildout.

Superior engineering. Superior product quality. Superior investment returns.

Semtech ( SMTC 0.00%↑ ) and Macom ( MTSI 0.00%↑ ) are both similar. They make various analog devices needed in communication systems.

Macom has a higher quality revenue mix from photodiodes.

Semtech has… LoRA junk… but they also have (allegedly) the industries best 200G/lane PAM4 linear equalizer (analog CTLE).

This gives Semtech insane torque to ACC, LPO, and MediaTek TPU. In the process of multi-sourcing the datasheet and writing up conclusions.

If you are risk-averse, Macom for you. I am buying both.

In my opinion, Coherent ( COHR 0.00%↑ ) is an inferior version of Lumentum. To play devil’s advocate, Coherent appears to have great yields on their ramping 6-inch InP wafer fabs. Given my crazy exposure to Lumentum (largest position in trading account) I am not touching Coherent.

The Chinese are represented by four main players in no particular order:

TFC ( $300394.SZ )

Accelink ( $002281.SZ )

Innolight ( $300308.SZ )

Eoptolink ( $300502.SZ )

Bluntly, the Chinese are at least 5 years ahead of the west when it comes to optics manufacturing. You have no idea how bad the gap is lmao.

These four are VERY GOOD at what they do, and the stocks should go up.

(I like TFC and Accelink the best.)

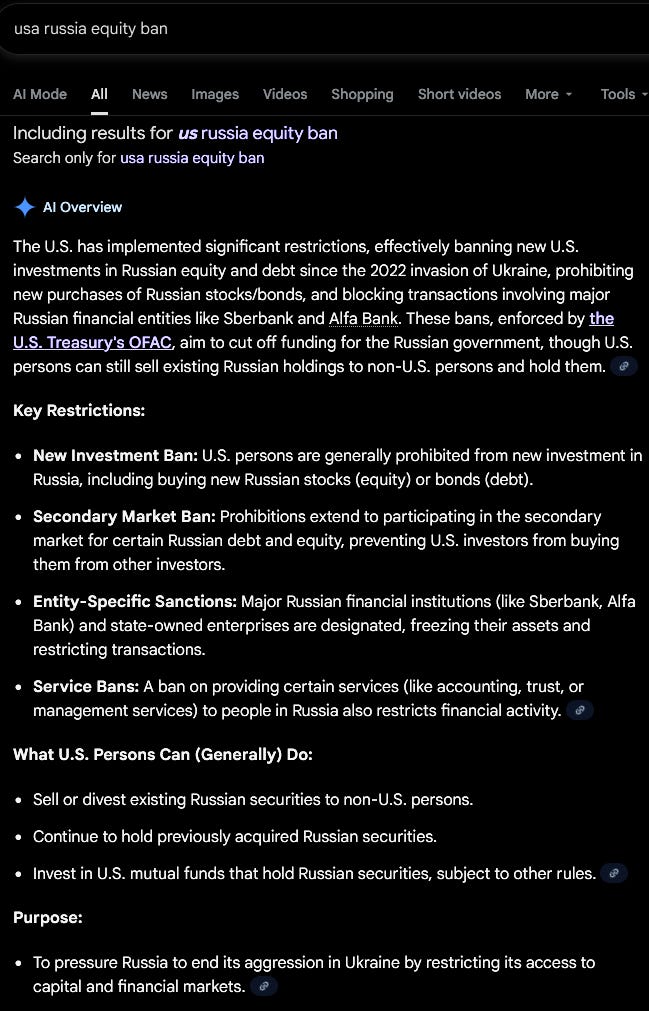

Now as for investing in these stocks, I am a USA resident and citizen. This makes it very dangerous for me to own Chinese-listed equities.

One executive order is all that is needed to wipe out the holdings. This already happened with Russia.

If you are an institution who is allowed to invest in Chinese-listed equities and has the lawyers to deal with trade war bullshit, go for it.

If you are a retail trader who resides outside of USA jurisdiction (PRC citizen/resident) also go for it. These four companies are exceptional in terms of competence, innovation, and ability to kick ass while making money.

For everyone else… there is Fabrinet ( FN 0.00%↑ ).

Fabrinet is THE ONLY WESTERN OPTICAL MANUFACTURING FIRM that can credibly match the Chinese in competence/quality/yield.

Literally this is all you need to know about Fabrinet.

Not Chinese.

Only competent/viable Non-Chinese options.

Speaking of competence, let’s talk about Applied Optoelectronics ( AAOI 0.00%↑ ), the… special member of western optics manufacturing.

These guys have a notorious reputation that has only recently improved. Credit where credit is due.

Their 800G transceivers finally got qualified by Amazon. If they can get 1.6T transceivers qualified, stock goes to the moon. If their new 400mw ultra-high-power lasers for CPO (recently announced) are any good, stock goes to the moon.

AAOI has huge internal laser production capacity.

Bluntly, I don’t want to deal with the chaos and volatility of this ticker. Have enough degenerate shit in my account.

But for the brave… AAOI could be great.

Finally, we have Furakawa Electric ( $5801.T ), a rather diversified firm.

Only some of the segments interest me. And they have gone to the moon lol.

Honestly, the way I found out and invested into this stock is simple:

One of the hedge funds who talks to me asked for my opinion.

Never heard of Furukawa.

They told me elevator pitch.

Spent an hour browsing Furukawa website, saw some high-quality stuff, and decided to buy a bunch for long-only international account (Interactive Brokers).

High-quality fiber assemblies are difficult to make.

Tunable lasers (critical for R&D and industrial) VERY difficult to make.

Furukawa could start selling lasers for datacom eventually so another possible upside.

[2] Semicap

We need moar chips and the fabs need moar equipment.

Let’s start with Camtek ( CAMT 0.00%↑ ) and Onto ( ONTO 0.00%↑ ), the small-cap advanced packaging names.

Both are great. When you hear “CoWoS expansion” think of these two. But I like Camtek more because of geopolitical reasons.

Onto is an American firm who probably is afraid to sell into mainland China due to risk of getting a colonoscopy by the federal government.

Camtek is Israeli and gives zero fucks about selling to the Chinese.

So Camtek has more revenue opportunity. Bigger TAM.

Besi ( $BESI.AS ) is the king of hybrid bonding tools.

Hybrid bonding is critical for CPO (TSMC COUPE) and future advanced logic chips. Also HBM4 eventually. Spoke with a European institutional investor some time ago and apparently Besi is a popular funding short for EU hedgies.

Great tech, great market opportunity. Own a bunch in my Interactive Brokers account.

(no I don’t know anything about the Korean players and don’t care because I can’t own Koren equities)

Aehr ( AEHR 0.00%↑ ) is a name I have written a lot about. Please refer to this old post.

Same thesis as before.

Hyperscalers making degenerate decision to skip HTOL testing and just burn-in all the logic wafers lmao.

Heard from a few people the “hyperscaler” might be AMD?

Anyway, made a nice amount of money trading this ticker but no position right now.

Chart looks OK. Might buy back in. Been too focused on other things to give a shit about this agent of chaos.

Aixtron ( $AIXA.DE ) is a semicap company I have started to research because I want more exposure to optics but buying more Lumentum is retarded at this point.

Aixtron makes epitaxy machines critical for InP and GaN.

Guess who is gona buy a shit ton more equipment from Aixtron. (Lumentum, Coherent, fucking everyone)

I like this chart. Looks like opportunity to me.

Stock has traded like shit for 5 years because of SiC probably. (EV market)

Honestly this is good enough for me. Its a pain in the ass to do anything on Interactive Brokers dogshit UI but I will be buying some shares soon.

ATE (automated test equipment) is a special (almost) duopoly between Advantest ( $6857.T ) and Teradyne ( TER 0.00%↑ ).

For years, Advantest has been repeatedly humiliating Teradyne in high-per (HPC) testing. Ter seems to be making a modest comeback, has exposure to memory testing, and has the robotics thing Citrini highlighted.

Did an OK job trading Teradyne. No position now but might buy back in.

Finally, a new company, Nova ( NVMI 0.00%↑ ) gets some initial coverage at the request of a subscriber.

Primary competitor is KLA ( KLAC 0.00%↑ ) so uh ok you better have something good here.

Yooooo they publicly post papers on their website?

I understand nothing from these papers but massively respect Nova for dropping the standard cloak-and-dagger corporate bullshit and actually discussing engineering.

Gona buy some shares just because of this haha.

[3] Energy

Due to personal beliefs, I refuse to invest in any company that operates coal power plants. This bans Vistra ( VST 0.00%↑ ) and Talen ( TLN 0.00%↑ ), two popular independent power producers.

Constellation Energy is an IPP that is almost all nuclear.

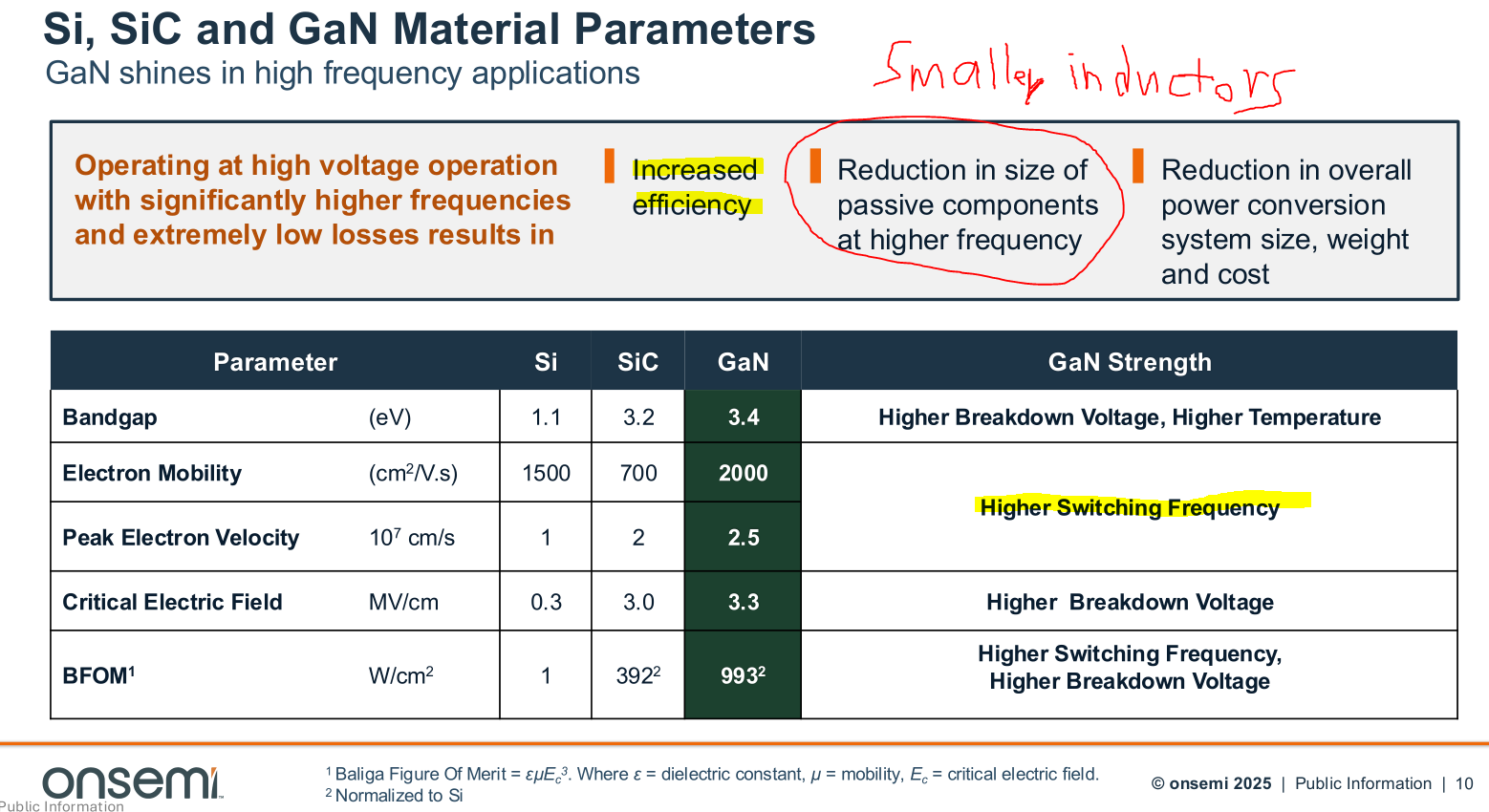

Within the world of power semis, there are a lot of degenerate options. It really is a shitshow out there. On Semi is a company that has been eating shit for some time because they are the primary SiC supplier to Tesla. As Tesla car sales go down (yet the stock goes up lmao) On Semi eats more shit.

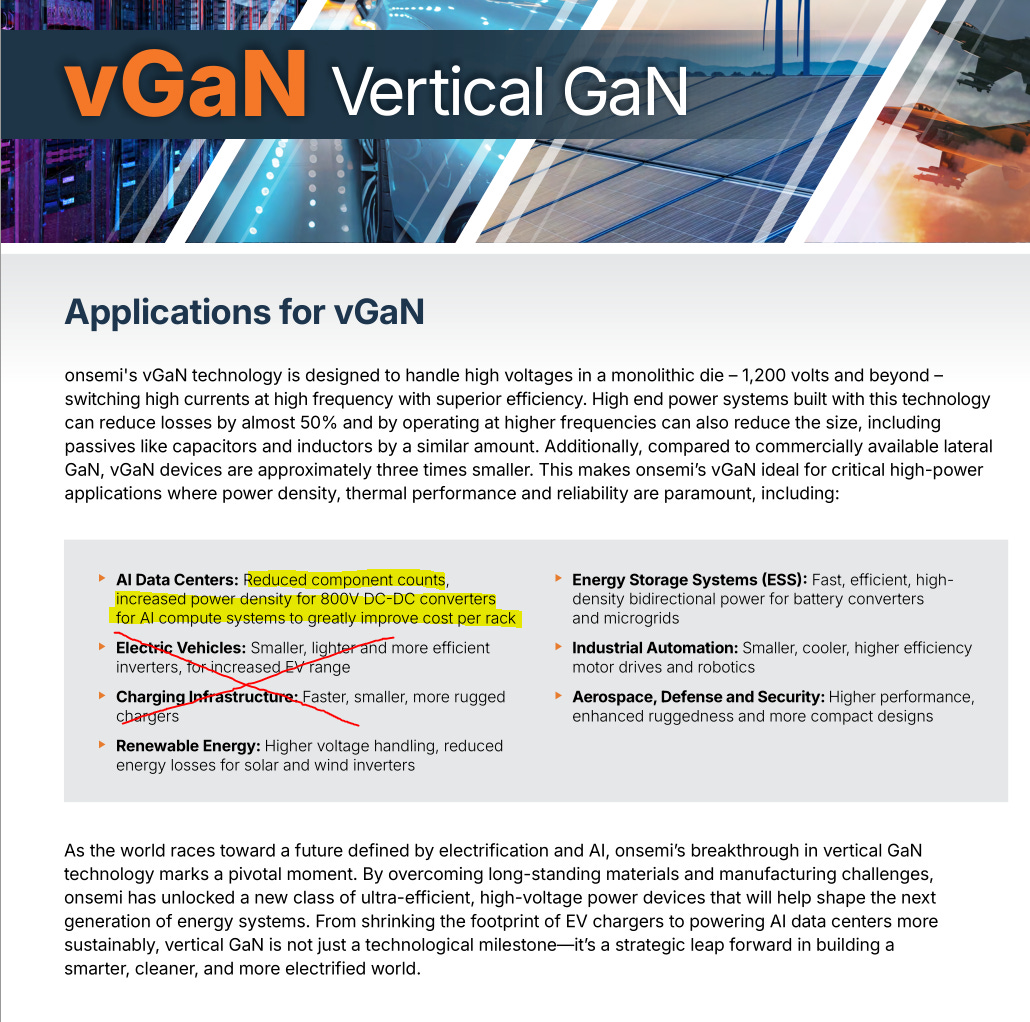

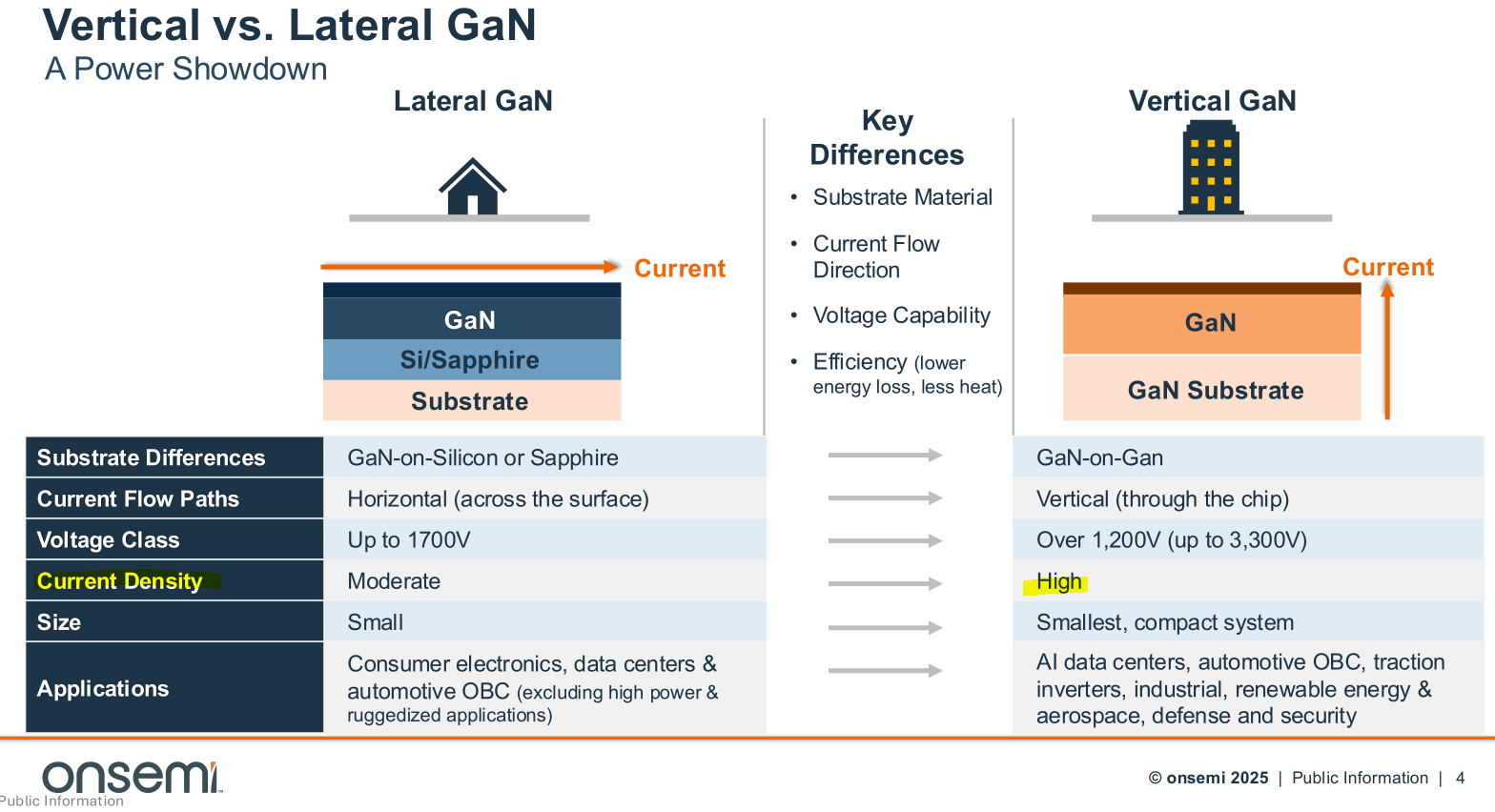

But a recent announcement of new GaN power semis caught my eye.

https://www.onsemi.com/solutions/technology/vertical-gan

Need more time to dig deeper and check the competitive landscape. Lots of people out there claiming same things.

But out of all the GaN power semi players, ON 0.00%↑ is the most credible. Stock getting murdered by Tesla SiC implosion makes this an attractive asymmetric opportunity.

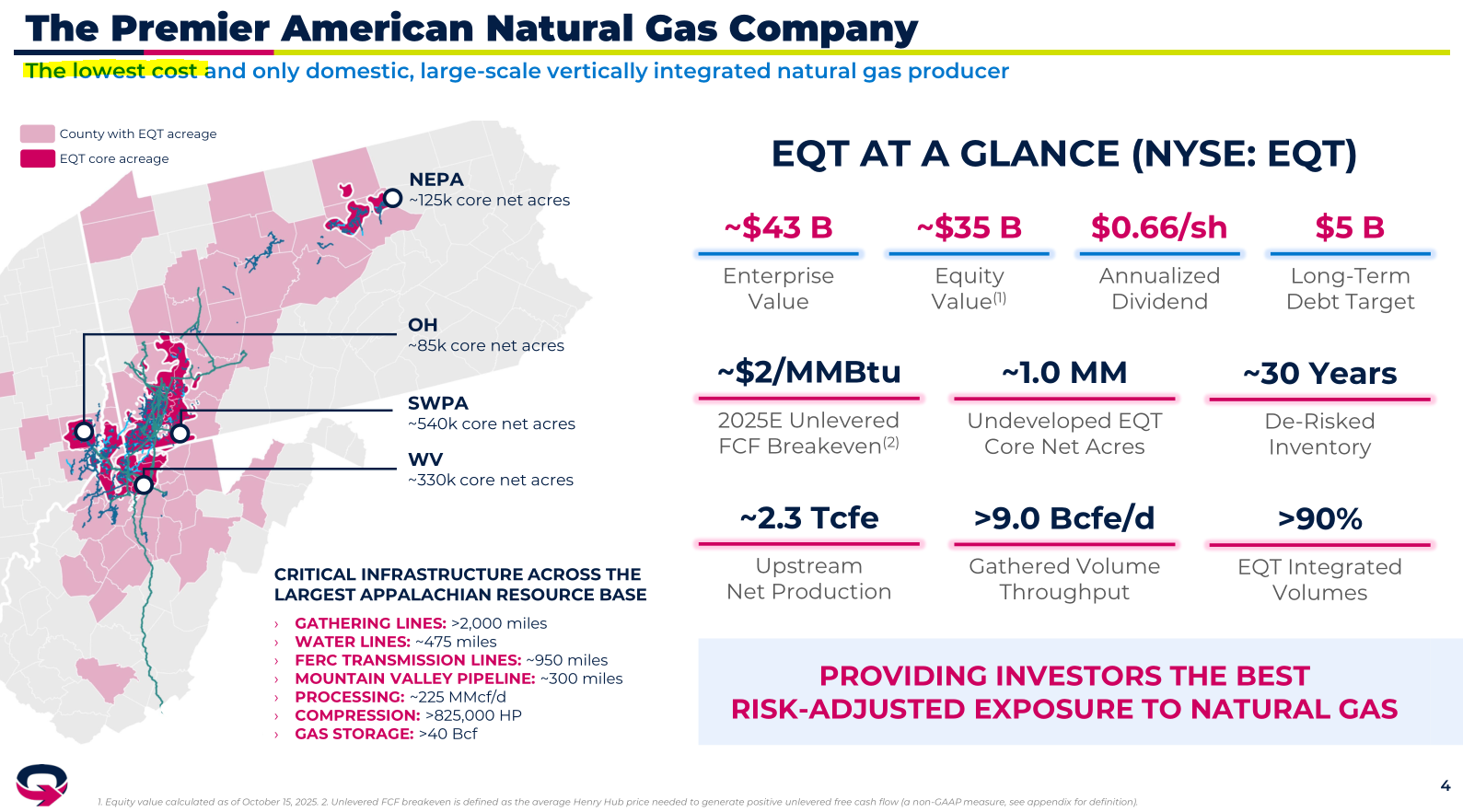

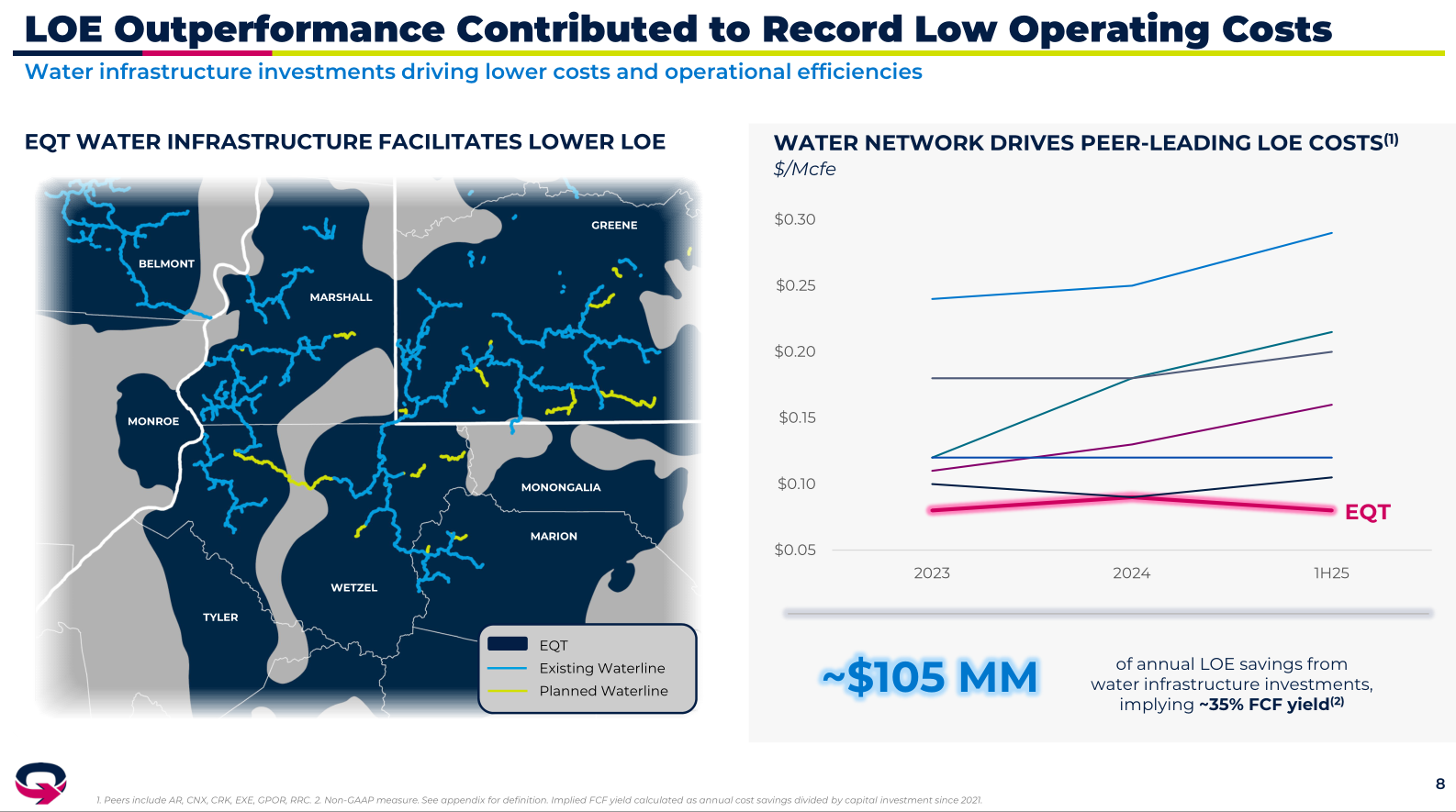

EQT 0.00%↑ is a natural gas supplier in the northeast USA. Unlike idiotic tree-hugging hippies, I am a realest and willing to tolerate natural gas which is WAY LESS DIRTY than coal.

In an ideal world, we would be ramping nuclear like crazy but the same tree-hugging morons shoot nuclear down because they lack a basic understanding of radiation.

Did you know living near a coal power plant exposes you to significantly more radiation than living near a nuclear power plant? kek

Natural gas industry has a reputation for being violently cyclical. EQT’s advantage is they are the cheapest and claim to be capable of surviving anything.

Also, I live in California and don’t care if people in Pennsylvania drink poisonous water from fracking. Messa supporting your local economy!

What do they need all that water infrastructure for you might be thinking?

(hydraulic fracking ayyyy lmao)

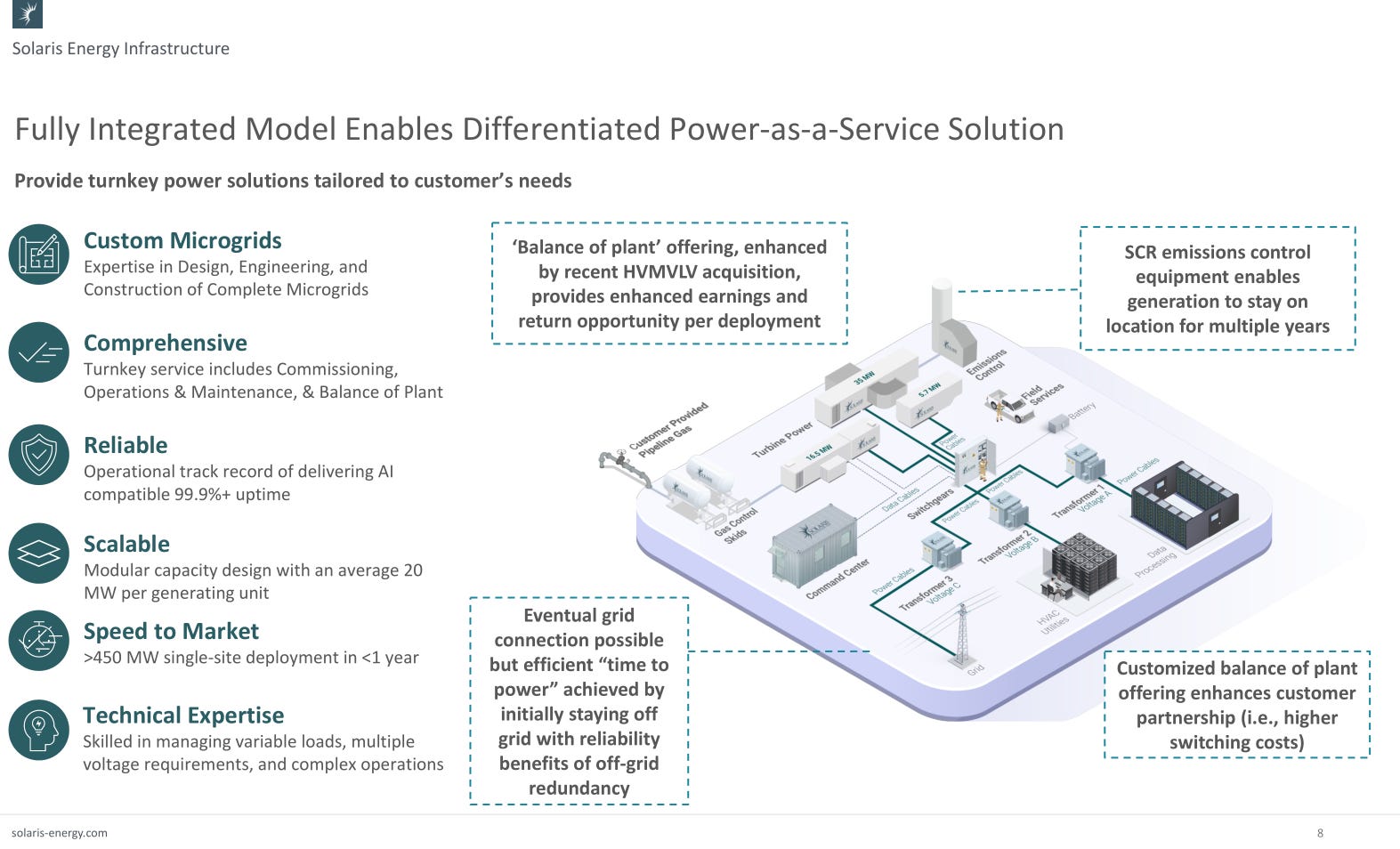

Final two energy ideas are Solaris Energy ( SEI 0.00%↑ ) and Bloom Energy ( BE 0.00%↑ ), both related to “time to power”.

Do you want to power up a datacenter without waiting like at least one year for regulatory approval or other bottlenecks?

Solaris will cart in a fleet of mobile natural gas generators and set up a pseudo-organized local grid.

Bloom makes fuel cells. Natural gas goes in, undergoes a chemical process that IS NOT BURNING, and energy comes out.

OutspokenGeek has a glorious post and you should go read it.

What caught my interest is 800V DC direct to datacenter. First found out about this at OCP and you can see coverage of entire conference here.

Skipping DC-AC and AC-DC conversion is huge. The more I think about this, the more exciting it becomes. These fuel cells have a real chance of going from niche solution that only viable in power shortage to THE superior solution on merit.

Waiting for wash sale rule to pass before buying back in. I fucked up trading this. Viewed Bloom as highest risk holding and liquidated multiple times in panic de-levering maneuvers.

[4] Timing

Frequency Electronics ( FEIM 0.00%↑ ) makes rubidium clocks.

Most clocks are made with quartz crystals that vibrate.

Ultra high-precision clocks are typically made with selenium or rubidium.

Imagine paying $1M for a clock. Who is gona buy that?

Military.

High-end phased arrays used for military applications need this kind of precision. FEIM is basically a pure-play military spending name without any ethical issues.

Botched the timing on this one. Sold and took tiny profit before they announced massive backlog and stock mooned. Not sure if I want to chase this.

SiTime ( SITM 0.00%↑ ) is a company I have covered extensively in the past. Been harassing them about jitter but… seems they finally fixed the problem.

Have a huge deep-dive partially finished in drafts folder…

They have new parts that have 80 fs jitter using the correct measurement methodology. If they get that number down to 40-60, quartz is dead.

FYI a good quartz part can hit 35 fs jitter nominal.

[5] Logic Fab

Skywater ( SKYT 0.00%↑ ) is a mediocre logic fab with 130nm and 90nm class nodes. They are a military pure-play. Austin Lyons has excellent coverage and you should go read his post.

Quick comments…

GloFo is foreign owned.

Intel has no external PDK for old (dirt cheap) nodes. At best, a 22nm-class node will come online with UMC help at some point.

If you are USA military and need cheap/old chips for basic stuff… Skywater really is the only option.

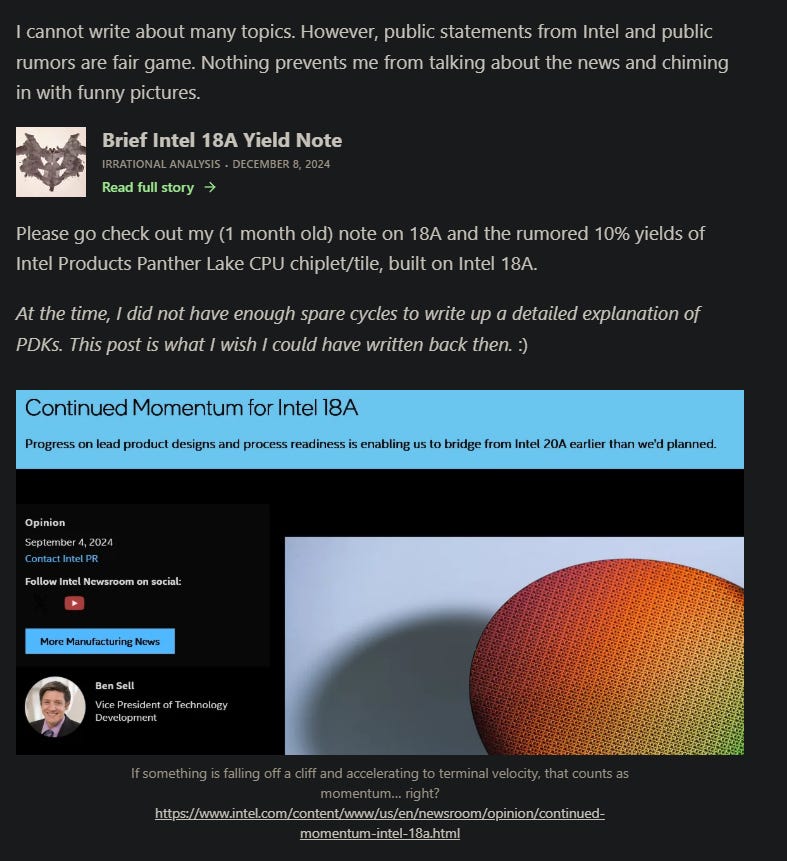

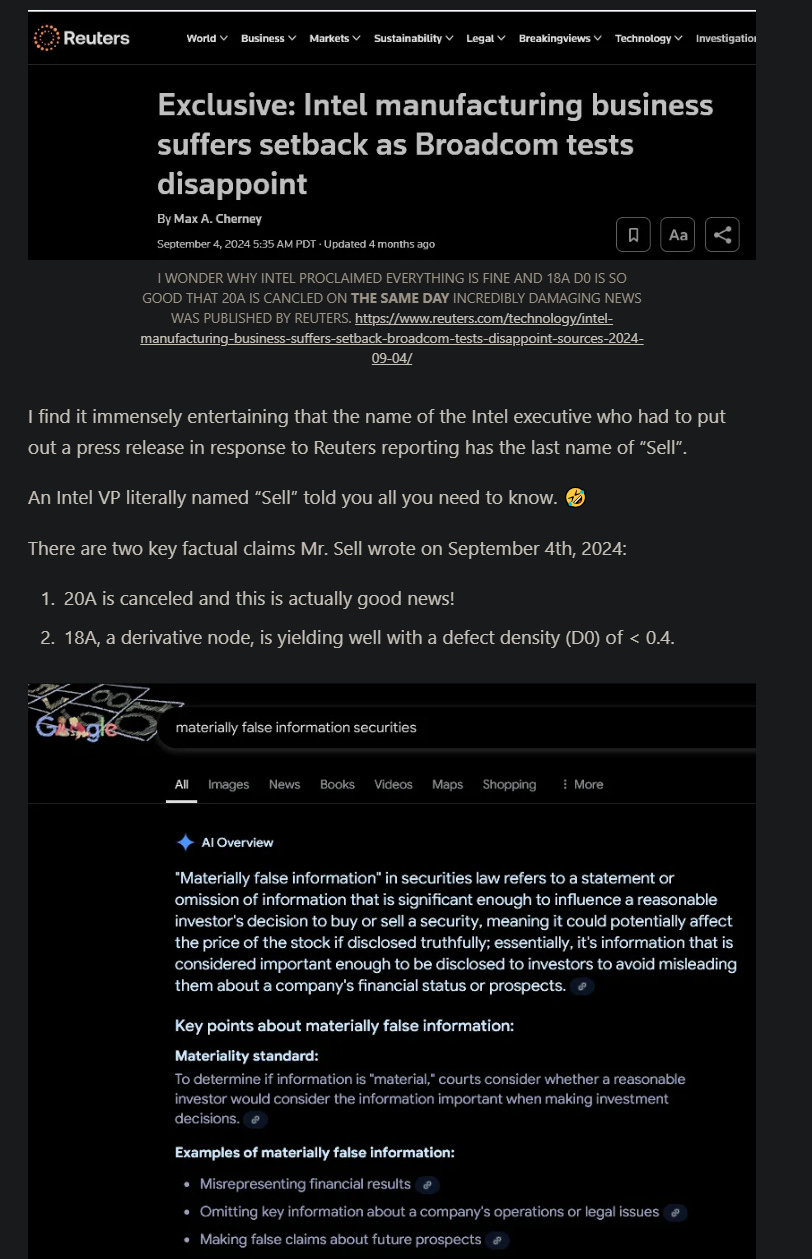

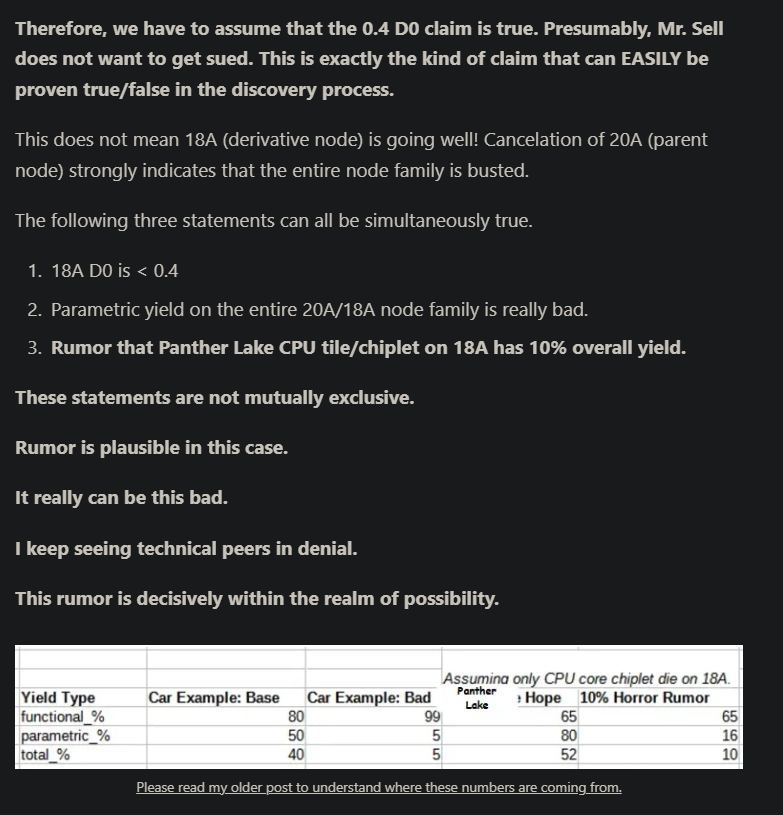

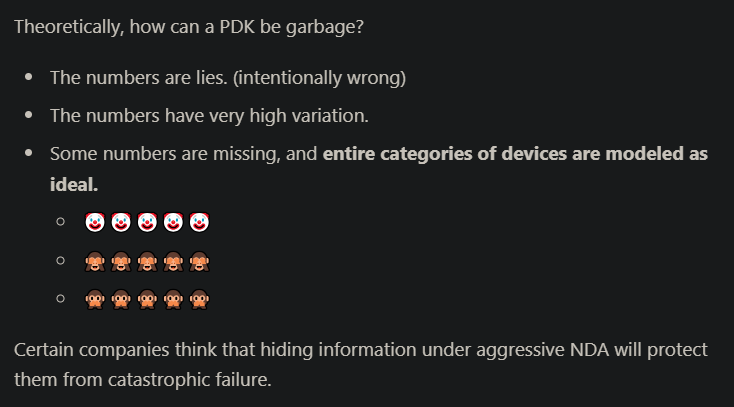

Intel ( INTC 0.00%↑ ) has gotten extensive coverage.

Wrote a huge guide on process development kits to not-so-subtely shit on 18A PDK.

I was completely right on 18A being utter dogshit. Like for an entire year as others blindly believed in bullshit IEDM papers and cope.

Things are turning around though. 18AP is essentially a fixed version of 18A.

14A rumors don’t matter. It is way too early.

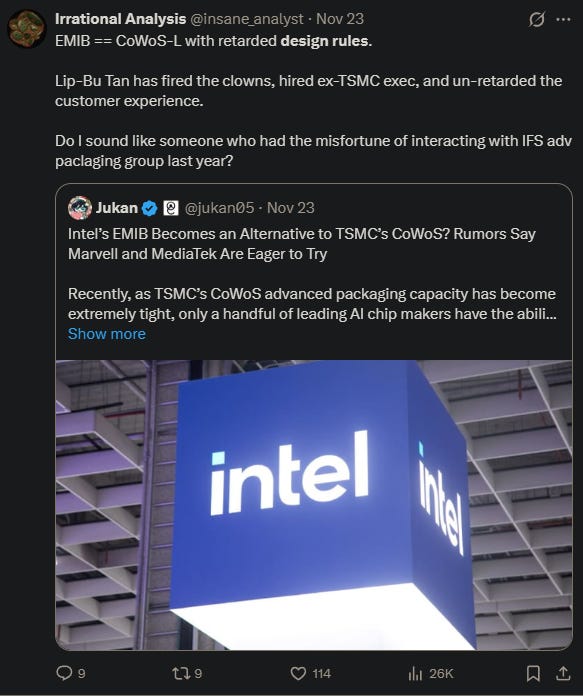

18AP is going very well given the public rumors, Apple rumor being the best one. Advanced packaging is a huge opportunity for IFS and they appear to have finally removed head from ass.

So now we have to talk about valuation.

I do not care about Intel Products. Probably dead within 5-10 years.

Fab is all that matters. The world needs a credible competitor to TSMC in high-end logic and IFS is it.

Global Foundries, a trash fab with a collection of trash nodes nobody wants trades at 1.7x price/book.

Intel, the 2nd place leading edge fab undergoing a historic turnaround, trades at 1.65x price/book.

What the fuck guys? Either GloFo is comically over-valued, or Intel is comically under-valued.

Intel deserves 2x price/book of GloFo. (I know Intel’s book is on fire right now)

Again, I don’t give a shit about Intel Products. Honestly, Lip-Bu Tan has been too kind. Should have fired 50-70% in Hock Tan style.

For some reason, the older 7nm-class CPUs are selling very well so… horary short-term cashflow to feed the fabs.

Also, I hate the SambaNova deal. Congrats to the SN people for getting bailed out but it should not have come from Intel. That $1.6B should got to fabs.

Lip-Bu Tan is doing a great job and I guess some mild self-dealing (bailing out one of his VC portfolio companies) is acceptable.

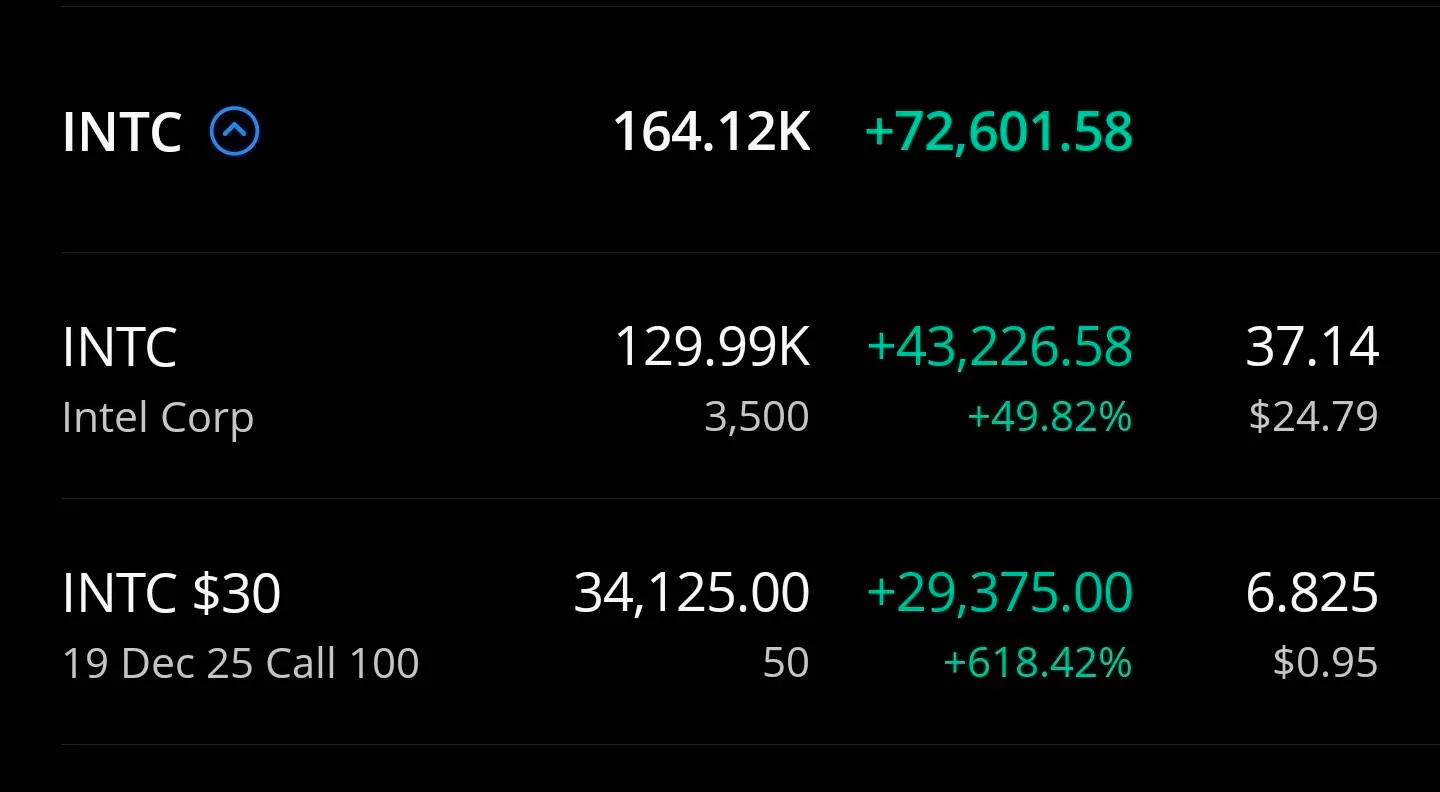

Own a shit ton of Intel stock.

All those options are expired on Friday and become shares on Monday. I effectively own $315K worth of shares at the time of writing.

#3 holding in trading account. I think #4 overall holding.

[6] Miscellaneous Longs

High-end PCBs are under a massive shortage. All the Taiwan players are sold out. Manufacturing high-end PCBs that can handle high-speed (100G+) signals are difficult to make. TTMI 0.00%↑ is one of the few non-Taiwan players. They also make PCBs for USA military. Worth a look.

Keysight ( KEYS 0.00%↑ ) I have covered several times. It is by far the safest datacenter/AI play. Super duper omega moat. If I see one more sell-side note that claims “test and measurement” is fragmented I will scream.

Dumbasses have you ever used ANY the following instruments…?

Sampling scope

Real-time scope

Spectrum analyzer

Network analyzer

Time-domain reflectometer

Arbitrary waveform generator

Wireless call box

Channel emulator

Bit-error rate tester

… across multiple vendors in the space that compete with Keysight such as…

Tektronix

Arnitsu

R&S

Teledyne

Rigol

No?

Why don’t you shut the fuck up?

Keysight’s competitors regularly quote half price in critical categories and still lose because Keysight’ competitors products are unusable dogshit.

Keysight’s moat is full of the rotting corpses of the “fragmented test and measurement” market.

Memory is the most degenerate sub-sector within semiconductors.

NAND flash is the most degenerate sub-sector within memory.

Made a nice amount of money trading Sandisk ( SNDK 0.00%↑ ) and frankly afraid to jump back in.

Look at this chart.

You see that sell at the top around $265?

Funny story. Was checking the trading account and saw that largest position was Broadcom. Ok.

Second largest position… Sandisk… not ok lmao.

Sold half on the spot. sold other half as entire market shit itself as part of a panic de-leveraging maneuver.

Musashi Seimitsu ( $7220.T ) makes super-capacitors.

Think giant capacitor that acts like a battery and a filtering cap at the same time.

Read all the datasheets for supercap vendors and Musashi is WAY ahead. Not even close.

As AI racks become higher power density, supercaps are needed to smooth out DC voltage ripple.

[7] Funding and Tactical Shorts

A surprising number of subscribers are hedge fund people. Learned that many hedge funds must short something to be factor neutral.

For example, can’t buy Nvidia stock. Have to sell short some AMD stock for example to fund the Nvidia position.

Here is a menu of five funding shorts for your amusement:

Qualcomm ( QCOM 0.00%↑ ) I have written about extensivly.

Nothing has changed. The Cloud AI 200/250 bullshit announcement will amount to nothing. Looking forward to the Q1 event that actually gives details.

Shorting QCOM 0.00%↑ and going long literally any other large-cap semiconductor stock will work as a pair trade.

Arista ( ANET 0.00%↑ ) has a problem. Someone is coming after their gross margins.

They have a website.

Shorting Arista and going long Broadcom probably works?

Credo ( CRDO 0.00%↑ ) has an insane valuation because Marvell has botched the time-to-market of their Alaska AEC chip.

At some point in 2026, Marvell will figure out… whatever is going on… and vaporize Credo’s gross margins.

Additionally, proliferation of ACC might shrink the expected TAM for Credo AEC.

Pairing a short of Credo with long (Semtech, Macon, Marvell) is worth exploring.

I hate Astera Labs ( ALAB 0.00%↑ ), a meme company that re-packages Synopsys SerDes for Amazon.

There are a bunch of people at Annapurna/Amazon who own a shit ton of ALAB stock and thus have strong incentive to give them ridiculous content.

Why yes use PCIe switching to reduce latency.

But also have an unhinged topology that needs crazy number of PCIe switches and multiple network hops, defeating the purpose of PCIe low-latency.

NIC side-car. LMAO

If Amazon picks NVLink fusion, Alab is in deep shit. All of the switching content goes bye bye. The content from Ualink/Nvlink retimers is not nearly high enough to meet whatever expectations retard buyside have.

No idea what to pair short ALAB with. I have tried to short these cockroaches 7 times and lost money every time. Maybe go long? The fuck do I know.

Global Foundries ( GFS 0.00%↑ ) sucks across all segments. If I worked at a hedge fund, I would 100% seriously pitch a MASSIVE short GFS, long TSEM.

It’s the perfect pair trade.

Cerebras ( $CBRS ) is going to IPO soon.

FINALLY.

Stay tuned I have lots to write about once the new S-1 filing is published.

Every fucking earnings call is going to get dedicated coverage.

Here is old coverage from the first IPO attempt:

[8] Dogshit (Neoclouds)

I hate neoclouds.

Debt-laden, degenerate, and the first to die when the market turns even slightly.

Instead of debating “AI is bubble” vs “AI is not bubble”, let’s take a reasonable and somewhat neutral perspective.

Semiconductors are a violently cyclical industry.

AI cloud is also a violently cyclical industry as the primary input is semiconductors.

The moment a minor downturn in the market, a road bump in demand, a small slowdown hits, 70% of entities on SEMINALYSIS CLUSTERMAX fucking dies.

Azure, AWS, and GCP are not stupid. (not completely stupid lol)

Satya Nadella has publicly said he is looking forward to buying cheap leases in the future.

Buying the corpses of his debt-ridden degenerate competitors.

Semianalysis own financial modeling shows how precarious these neoclouds financials are relative to hyperscalers.

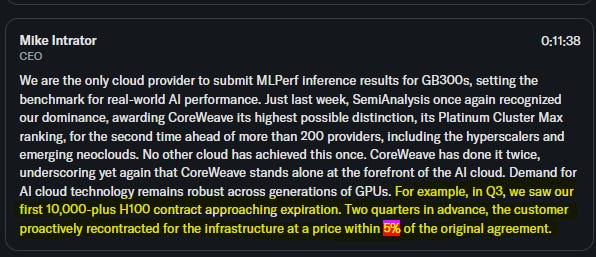

Let’s go over an example from the recent Corweave earnings call.

This datapoint that a 10K block of H100’s that were under (presumably) 3-year contract got renewed at a 5% discount to original price is useless.

Blackwell experienced 6+ months of delays due to (mostly) backplane issues.

To this day, Blackwell has many software and stability issues.

We are in a massive up-cycle… of course people gona renew Hopper contracts at favorable (to neocloud) prices.

At some point in the future, new generation hardware will so vastly out-perform the old generation that a supply shock (token capacity inflation) will cripple already shit pricing power from the cloud providers.

In other words, generation N+1 obsoletes gen N-1 and severely diminishes gen N profitability.

My guess is within the next 1.5-3 years. This means I think everything will be fine for next 18 months to be clear.

Do you seriously think Nvidia/AMD/Hyperscalers are willing to slow down product roadmaps to allow industry to digest a temporary token glut? NO!

In a power-constrained environment, it is logical for neoclouds and hyperscalers to upgrade IT hardware early. This is an epic prisoners dilemma. If everyone chooses to not upgrade, then everyone gets to stay on planned depreciation schedule.

But someday, an extinction-level event is going to obliterate vast majority of the neoclouds. SEMIANALYSIS CLUSTERMAX 15.0 is gona be awfully empty lmao.

To an extent, investing (especially my style of investing) is a form of gambling. There are risks and uncertainties. and often luck is a major factor.

But not all gambling is equal.

Poker is a game of skill where the top 1% of players take most of the winnings because skill (reading people, calculating probabilities) is a major factor.

Blackjack can be a game of skill via card counting. Casinos have gotten much better at catching and banning card counters though.

Slot machines are the opposite. Zero skill. You punch button and a machine (which is literally programmed to take your money) decides the outcome. Slots are the dumbest form of gambling in my opinion.

Here is my record on slots this year:

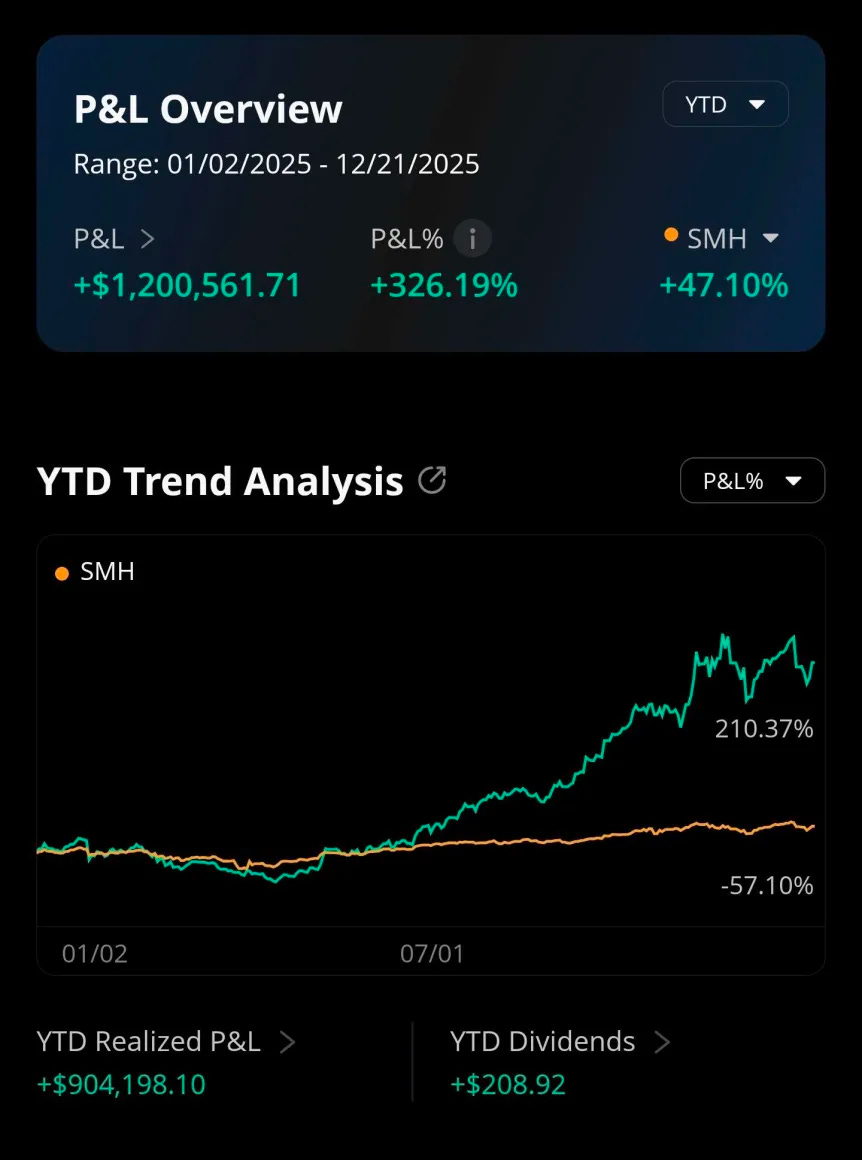

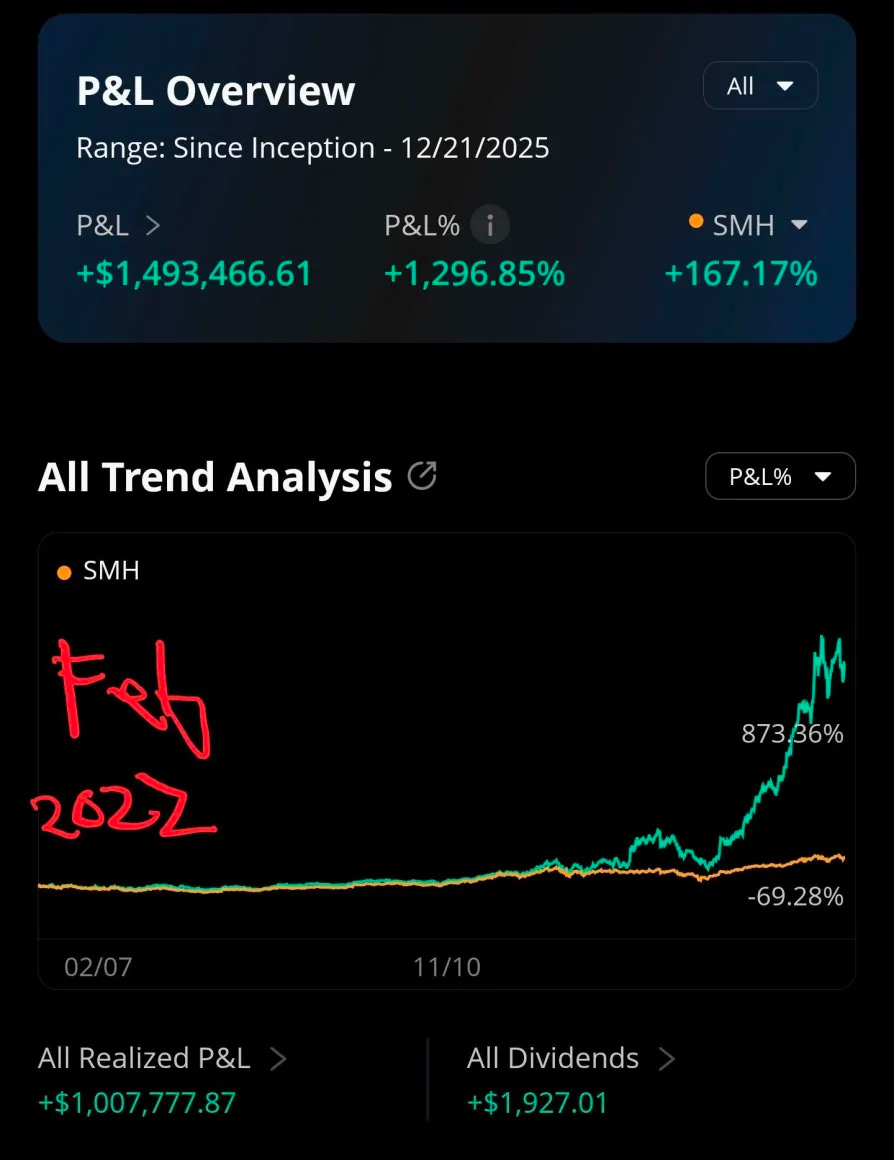

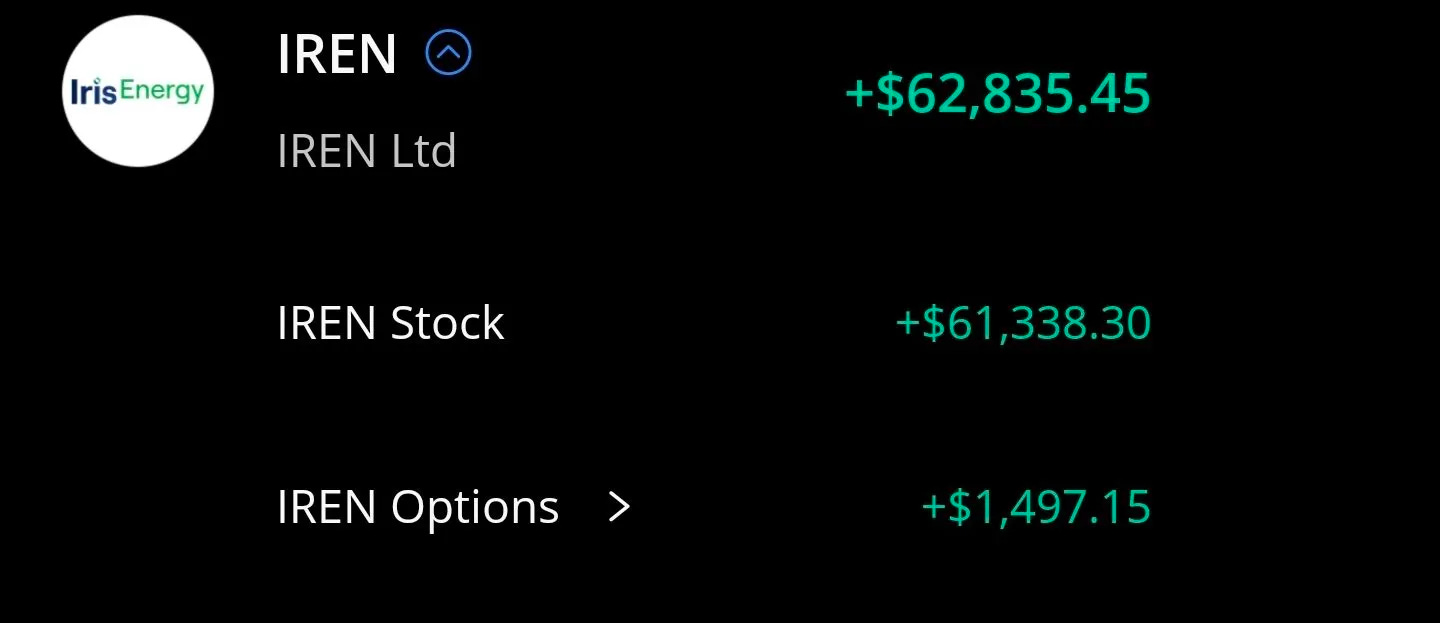

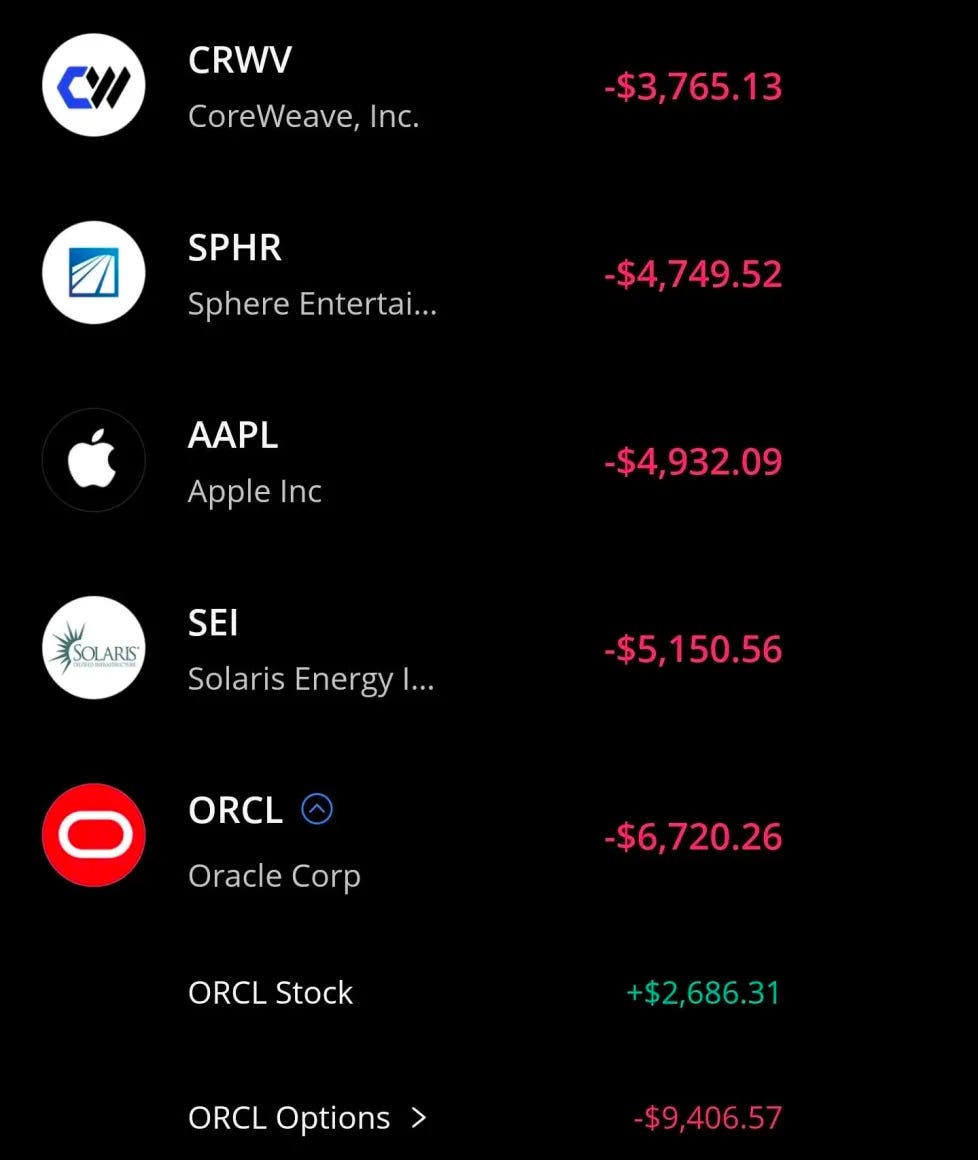

In 2025, I am net +$21K on trading dogshit.

If slots are your idea of fun, go for it.

Just don’t think these neoclouds and miners are anything serious.

$/MW of critical IT capacity… lol

As an aside, Oracle ( ORCL 0.00%↑ ) is probably too big to fail and Larry has CIA connections so might be worth a trade.

[9] Marvell (they get their own category lmao)

Marvell ( MRVL 0.00%↑ ) is special. By far the most controversial stock in semiconductors. The hedge funds are OBSESSED with this ticker.

Let’s start with Celestial AI acquisition. Technical coverage here.

For the lazy, I have prepared a fun analogy.

To explain Matt Murphy’s decision to acquire Celestial AI, lets go to a F1 analogy because a friend of mine will find this hilarious.

You are Matt Murphy, the driver of team Marvell.

Your car is shit. You are basically guaranteed to lose every race in the upcoming season.

One night, after a disastrous practice race, a shady figure in a trench coat approaches you and offers a deal.

In exchange for $3.8B in cash and equity, you get a new car that has two possible outcomes each race:

A (100-X)% chance you finish top 3 in the race.

A X% chance the special car blows up, kills you and the entire pit crew as well for good measure.

The fun part is nobody knows what X is, not even the mysterious trenchcoat-clad salesman.

Could be 0.0001%.

Could be 1%.

Could be 50%.

I am so excited to see what happens in the 2028 season!

To be abundantly clear, I am not claiming what number X is. All I am claiming is two very distinct outcomes are possible, and nothing in between.

Serious discussion now… Marvell really is a combination of contradictions.

The Alaska AEC chip is excellent, but time to market has been poor.

800G optical DSP is industry-standard (80%+ share) and a massive ramp is happening next year, but Marvell is losing huge share on next-gen 1.6T optical DSP.

Trainium 3+4 content is almost completely gone. Everyone knows this except Harlan lmao.

Fine, maybe some light back-end work. Amazon account is falling off a cliff. Extra Trainium 2 orders and some scraps of Trainium 3/4 will not support buyside expectations. If anyone actually believes Harlan… lol stock is not appropriately priced. Celestial AI deal is partially to re-acquire Amazon as a customer for Trainium 5/6/7.

Microsoft ASIC program is an unmitigated disaster. Mostly Microsoft’s fault. They are talking to Broadcom seriously for ASIC services. MSFT 0.00%↑ has the RTL source code for OpenAI ASIC! They can just ask Broadcom to make a derivative of OpenAI chip lol.

Datacenter switching is going to the moon, but Marvell switches (via Innovium acquisition) are missing in action. Most of the Innovium team now works at a startup called Upscale AI…

Anyway, may your 2026 trading be profitable. Or at least amusing.

Sometimes, losing money is fun.

Fking good annalysis! but sometiems, I'll do opposite direction lol

love this shit. finally something fun to read! good luck in '26. thanks for the insights.