Consider this a part #1.5 while I finish part #2. Goal is this December but it depends.

ARM (LTD) had their first earnings call since going public post-Softbank.

Companies with AI exposure did just fine this week. :)

It did not go well.

Let’s start with the shareholder letter.

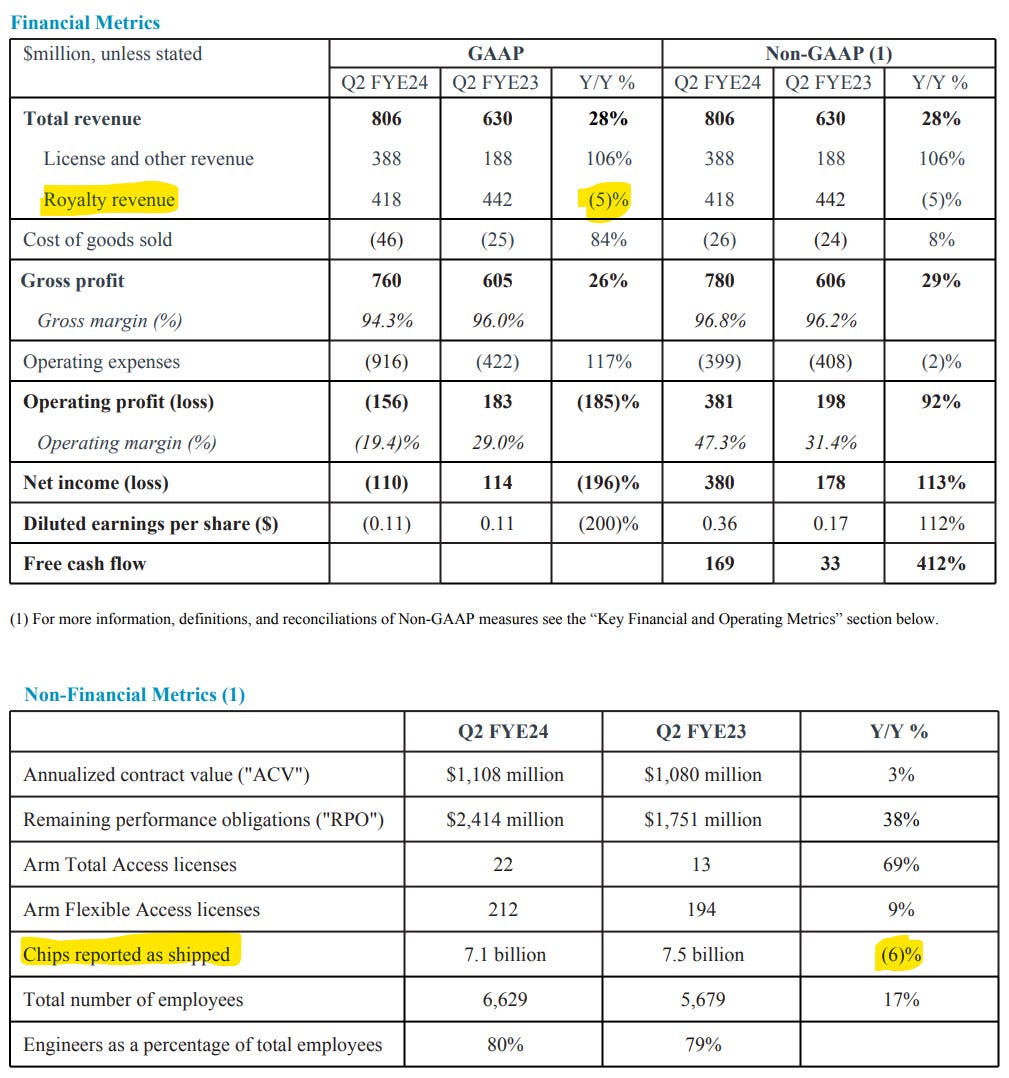

The vast majority of ARM royalty revenue comes from smartphone and low-end embedded markets. This is why the average royalty per chip is only six cents.

Around half of the decline (~200M chips) can be attributed to weak smartphone sales but the other half indicate share losses to RISC-V in embedded markets.

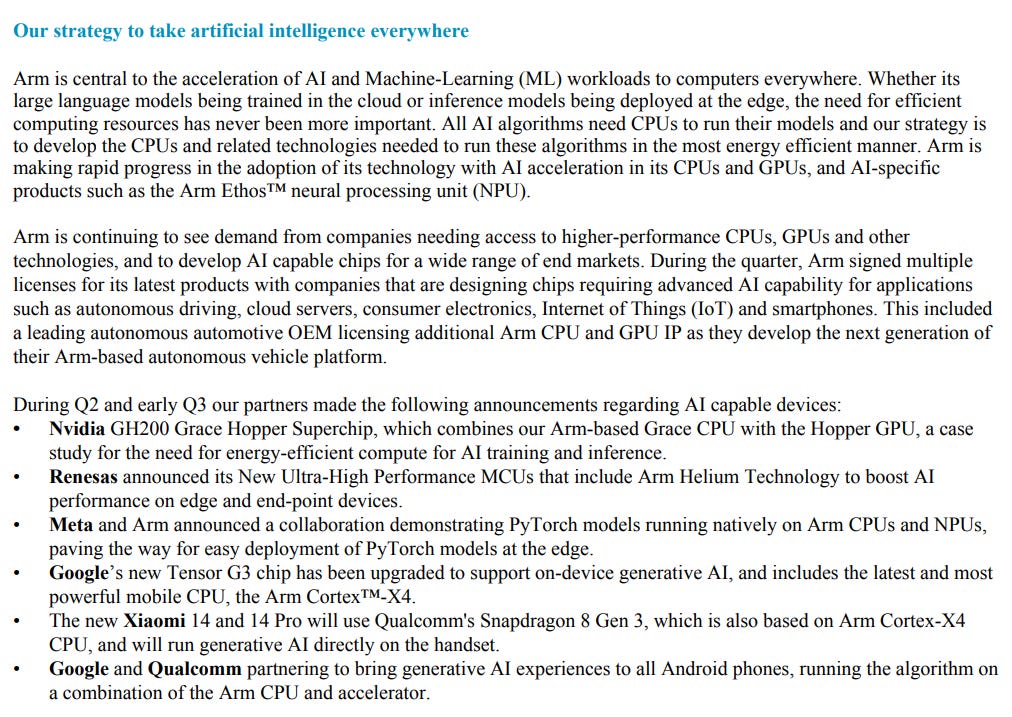

AI acceleration is all about moving the linear-algebra heavy workload off the CPU to dedicated accelerators. This entire section is nonsensical. CPU becomes a commoditized, low-priority block in AI workloads. ARM had a NPU program but gutted it while Softbank was trying to unload shares upon public markets. Now, Intel, AMD, Qualcomm, Apple, Samsung, Huawei/HiSilicon, MediaTek, and Google all have their own NPUs that use proprietary VLIW or hidden RISC-V CPUs to control the matrix engines.

Nvidia: Grace CPU exists to run their software defined scheduler and feed the GPUs. ARM is capturing very little value from this deal because of the sweetheart deal they signed with Nvidia during the acquisition attempt, according to SemiAnalysis.

Google: The Tensor G3 is running AI workloads on Google’s custom NPU! Cortex X4 contributes almost nothing to AI acceleration.

Xiaomi/SD8g3: Again, the AI acceleration is happening on Qualcomm’s Hexagon NPU and Adreno GPU. Qualcomm is going to have custom CPU cores for mobile by 2025 so ARM (RTL) // Cortex IP is getting 100% designed out soon.

Google and Qualcomm are both rushing to support RISC-V in Android and all those generative AI experiences run on accelerators, not ARM CPUs!

Neoverse CSS is essentially a CPU chiplet. They presented technical details at Hot Chips 2023. It is very interesting and I am trying to dig deeper for part #2.

ARM is trying to move up the value chain and this Neoverse CSS chiplet is the brightest spot in their business IMO.

Moving on to the earnings call…

Vivek Arya (Bank of America): Thanks for taking my question. Rene, for my first one, I'm curious. You had the IPO two months ago and the process started before that. What have been the big changes in your macro and industry assumptions, positive or negative, since the team went through that process? Any color by end market, geography? And specifically, what I'm trying to get to is that if you look at the way you were thinking about royalty revenues in December and the next few quarters, have they changed in any way, positive or negative, given any potential changes in your macro assumptions?

Rene Haas:

The reason ARM stock tanked after earnings was their weak guidance for next quarter. Beat in reported quarter was entirely due to lumpy licensing revenue. BoA analyst asked a very good question and ARM CEO outright refused to answer. In the pre-IPO roadshow, ARM management sold a royalty growth story to sell-side analysts, off the premise that they could raise prices. Given that Qualcomm is ditching Cortex CPUs in 2025 and Apple+Samsung are both exempt, I do not see this panning out. Huawei/HiSilicon is another huge headwind for the royalty hike thesis.

However, you just saw we've actually added about 1,000 people in the last year, and most of that is because of the headcount, mostly engineers, about 85% of those heads that we added in the last year are engineers.And those folks are specifically working on the compute subsystem, and the increased kind of complexity needed with all the designs that folks bought this quarter, and are going to forecast to buy in the coming quarters.

That is a lot of people. They must be working on something other than Neoverse CSS. A laptop compute chiplet is commercially unviable due to the limitations of Cortex CPU performance. Smartphone needs a modem and I doubt MediaTek would be willing to supply a discrete modem to ARM. Maybe Apple could sell their modem at cost to ARM to spite Qualcomm. Very curious to see what all these people are working on.

Chris Caso (Wolfe Research): Yes. Thank you. Good afternoon. The question is another one on AI and obviously a lot of discussion about AI capabilities and client devices. Can you go into a little more detail about how Arm monetizes that? Is it from a higher per chip royalty? Is it from a better mix at your customers, maybe some higher device ASPs? How do you see that playing out over time as AI gets embedded in client devices?

Rene Haas: Broadly speaking, the way I would think about it is whenever you're running one of these AI clients or assistants or agents, it's going to require a significant uptake in terms of compute capability, both in terms of if there's an in situ accelerator and/or through the CPU complex, keeping in mind that in a client device when you run these AI agents or whenever you're running something that's going to be a copilot of some sort, nobody wants to see their battery life suddenly go down 40% in terms of everything that was involved in running the algorithms. So what that means for us in the broad sense is I expect it's going to be a higher need for more compute capacity. We'll see more advanced cores. We'll see larger cores, more v9, which in the end game should mean higher royalty rates for us. That would be our belief going forward in terms of just the mega trend.

Frankly, this is a pipe dream. AI is all about moving the workload from inefficient CPUs (designed for out-of-order, branch prediction, superscalar..) to highly optimized dedicated hardware. AI is a mega trend against ARM.

John DiFucci: Okay, great. And second question. When we think about the guidance for next quarter and the year, obviously the macro backdraft has an effect, and you guys have your own crystal ball, I guess we all do, and it has an effect on both license and royalties. But the royalty part is really something you probably have less control over and visibility into that timing, even though there were a lot of questions here on license, which probably you have more visibility there. Jason, you did hit on the royalty visibility in one of the questions, but I just want to make sure I understand what's implied in guidance in regards to units – and I know there's a lot of other things that affect royalty revenue, most of which are going in the right direction. We can all see industry analysts' forecasts for units, and you guys have intimate relationships with your customers, so you can have even better visibility into that. But I'm just curious, when you look at industry analysts' estimates on units, so are you assuming about the same, a little below, or even perhaps a little even better, or do you just see things a little bit better than industry analyst estimates?

Jason Child: Sure. Okay, so here's what I would say. So in this quarter we just reported we were minus 5% on royalty. If I compare that to our three best comps, at least closest in terms of mix, you could look at MediaTek, you could look at Qualcomm, and you could look at TSMC. Those guys were all between minus 11 to minus 24%, as they just reported the last few weeks. So we had stronger growth than those guys, primarily because of our share gains that we're seeing in infra and auto, and then also in some part because – or in part because of the Armv9 adoption. So we are expecting that – and I think those guys as well as counterpoints from the other industry analysts, all seem to be kind of triangulating around flipping to positive sequential growth in this last quarter, and then in the current quarter, expecting to see that get kind of in the high-single digits approaching double-digit range. And that's pretty consistent with what we're expecting, and then same for Q4. So from everything I can see – and we do get paid royalties on 7 plus billion chips per quarter, so we do see quite a bit from a bunch of folks. As far as I can tell, we're kind of all triangulating relatively similar impacts. I think the difference probably are our v9 rates, maybe the piece to that is why we typically grow a little bit faster than maybe some of the others. Does that answer your question?

TSMC as a comp makes no sense. I strongly believe the soft royalty numbers are because RISC-V is gaining share within embedded markets.

If you enjoyed this content, please consider subscribing.