How Much is Ampere Computing Worth?

Valuation compared to an ARM Total Access License.

Irrational Analysis is heavily invested in the semiconductor industry.

Please check the ‘about’ page for a list of active positions.

Positions will change over time and are regularly updated.

Opinions are authors own and do not represent past, present, and/or future employers.

All content published on this newsletter is based on public information and independent research conducted since 2011.

This newsletter is not financial advice, and readers should always do their own research before investing in any security.

Feel free to contact me via email at: irrational_analysis@proton.me

Ampere Computing is out of money and desperate. Only the former is a new development.

Clearly, Oracle is not interested in acquiring Ampere Computing and further filling out their heavy bags. Otherwise, Ampere Computing would not be parading themselves in the press.

Contents:

How ARM Makes Money

Architectural License Agreement (ALA)

Technology License Agreement (TLA)

ARM Total Access License

ARM Flexible Access License

Neoverse Compute Subsystem (CSS)

Ampere Computing History and Status

Why is Oracle not buying Ampere Computing?

Deep Underwater

Assets

Liabilities

Rough Valuation Framework: VS ARM Total Access

[1] How ARM Makes Money

ARM 0.00%↑ has several ways that they monetize their IP. You cannot understand what is happening to Ampere Computing without first understanding ARM and what an instruction set architecture (ISA) is.

For a detailed walkthrough of instruction sets, refer to the above linked post.

In short, ARM (ISA), x86, and RISC-V are all just languages. Analogous to English, Spanish, Mandarin, Arabic, … and so on.

The difference is… computer languages are IP that are often monetized.

x86 is only available to INTC 0.00%↑ and AMD 0.00%↑ due to historical reasons.

Technically, there is one Chinese company (Zhaoxin) with access to x86 ISA but they are so behind it does not matter.

ARM (ISA) is available to whoever is willing to pay ARM (the corporation) for a license.

RISC-V is free and open-source.

Instruction sets also have versions. ARM management often discusses how their royalty rates for V9 architecture is much higher than V8.

Imagine you have a license to write English novels with a limited vocabulary, only using slang, idioms, and words from the 1920’s.

It would be nice, but not strictly required, to have access to the latest superset of words, idioms, and slang.

In a nutshell, this is what the difference is between ARM V9 and V8. More features, updated rules, better efficiency and performance enabled by the latest version of the computer language.

While possible to drag your feet and stay on ARM V8 for as long as possible (Apple only recently moved to V9 and Qualcomm/Nuvia is staying on V8 because lawsuit), this strategy becomes untenable over time.

Ampere Computing is on ARM V8.6 at the moment, and thus far behind ARM (the corporation’s) own offerings.

Of course, having a license to the computer language is not useful by itself. You need to design a CPU core (write the novel).

With that, let’s break down all the ways ARM (the corporation) makes money and by extension, all the ways Ampere Computing’s former customers are ditching them and directly working with ARM to build their own cloud-native chips.

[1.a] Architectural License Agreement (ALA)

Customer pays ARM (the corporation) a one-time, up-front license fee for the right to use a specific version of the ARM ISA. Typically, an ALA covers an entire family (V8, 8.1, 8.2, …) and has the lowest royalty rate of the ARM licensing options.

For example, Apple paid for a V8 ALA a long time ago and designs thier own CPU microarchitecture (IP) in-house. Apple also pays ARM approximately 30 cents per chip royalty upon manufacturing. The latest iPhone 16 SoC uses ARM V9 and commands a higher royalty rate per chip.

[1.b] Technology License Agreement (TLA)

What if you don’t want to write your own novel and prefer a just buy a manuscript and print your own books? ARM has you covered with a TLA. ARM designs and sells their own CPU cores under the Cortex brand (X3, N2, V3, A710, A520, M4, ….).

The letters denote the target market.

Datacenter: V/N/E

Mobile: X/A

Embedded: M/R

TLAs have a much higher royalty rate per chip produced compared to an ALA. Additionally, the up-front TLA license fee is much lower than an ALA. Tradeoffs!

Importantly, TLAs are for specific core designs. One TLA for an X3, another TLA for an A-520, and so on.

[1.c] ARM Total Access License

Suppose you want access to every IP block ARM has, from the latest V9 versions all the way to ancient V7 stuff.

In exchange for an expensive annual subscription (not one-time/perpetual license!) you can.

[1.d] ARM Flexible Access License

Another annual subscription but cheaper than Total Access with some of the latest IP unavailable. I suspect V9 is excluded but there is no public confirmation on where the cutoff is. Some old V9 IP might be in this license. Not sure.

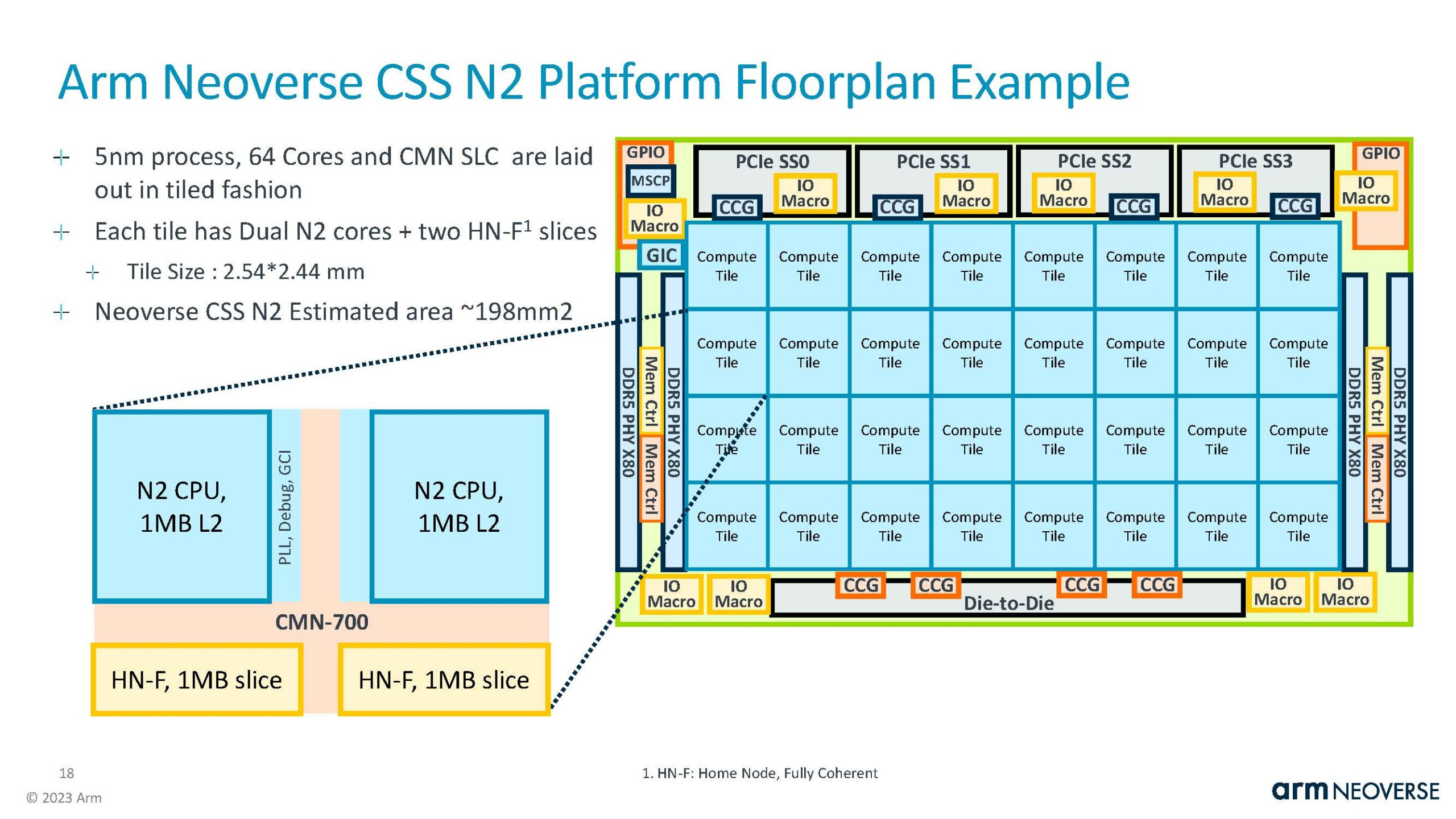

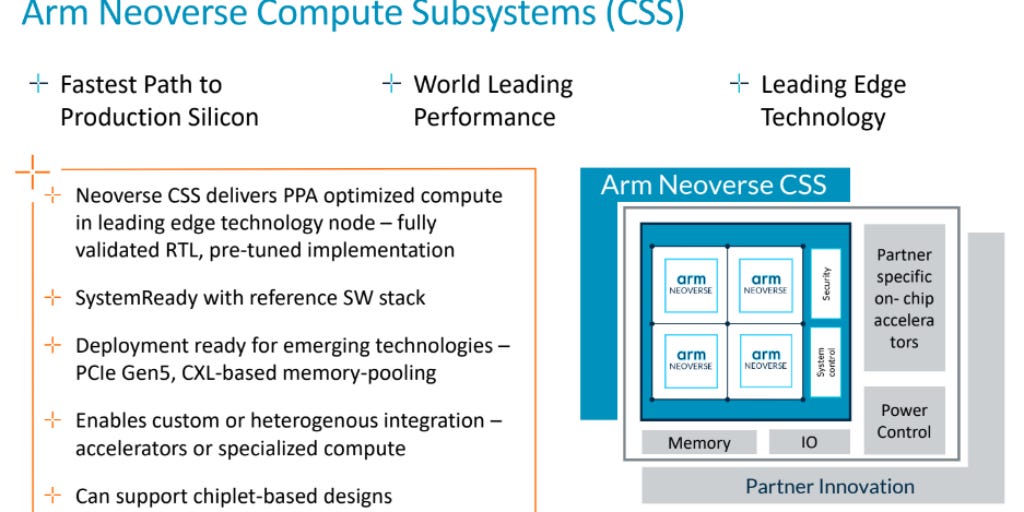

[1.e] Neoverse Compute Subsystem (CSS)

What if you are so lazy you don’t even want to buy a manuscript and print books. Why not buy books (complete chiplets with full physical design and validation)?

You can!

Microsoft Cobalt (one of many former Ampere Computing customers) is built using ARM Neoverse CSS chiplets.

[2] Ampere Computing History and Status

Ampere Computing is a startup that was founded by Renee James and several other ex-Intel folks back in 2017. There was some initial success with their “cloud-native” (manycore, consistent performance, low-power) solution. Great customer traction.

Back then, many industry analysts (myself included), wondered if the big clouds were buying these Ampere Computing chips for long-term use or if they just wanted to port their software from x86 to ARM (ISA) and then dump Ampere.

The latter turns out to be what is playing out.

At one point, Softbank proposed to value Ampere Computing at $8B. Shortly after, Ampere Computing tried to IPO but backed out because that is when their revenue started imploding as customers ditched them and just worked directly with ARM.

Quick observations:

Daddy Oracle has dumped a lot of money into this failed company.

The last funding round was way back in April, 2022. Over two years ago!

Around $800M has been invested into Ampere Computing.

(did Softbank multiply invested capital by 10 for their $8B proposed round in 2022???)

But wait… it gets funnier!

Guess who is on Oracle’s board?

Because Renee James is on Oracle’s board, ORCL 0.00%↑ is legally obligated to disclose how much they invest in Ampere Computing and how much they purchase too. Investments and prepayments from related parties! HAHAHAHAHAHA

The 2024 proxy statement from Oracle will have updated info. It would be interesting if we already did not have overwhelming evidence that Ampere Computing is a corpse desperately parading itself for suitors via Bloomberg.

[3] Why is Oracle not buying Ampere Computing?

An obvious question many of you might be thinking.

The main reason is… Oracle gains nothing incremental from a full buy-out. They are well aware that they are Ampere Computing’s last remaining source of meaningful revenue.

Presumably, Oracle has signed some kind of long-term contract/agreement with Ampere Computing. That would explain why the old generation chips will get guaranteed support through 2030.

Ampere Computing has no choice but to accept whatever ASP Oracle (their only customer) is willing to pay. Liabilities (in the form of prepayment and support contracts) likely outweigh the remaining non-Oracle equity value.

[4] Deep Underwater

At Hot Chips, I was discussing Ampere Computing with someone who I respect deeply. My argument was they are a zero and worthless. His stance (which is correct) is that they must be worth something. IP has to be worth something.

So instead of making some memes and claiming Ampere Computing is a zero (extremist opinion), let me try to be fair and value them at some nonzero number.

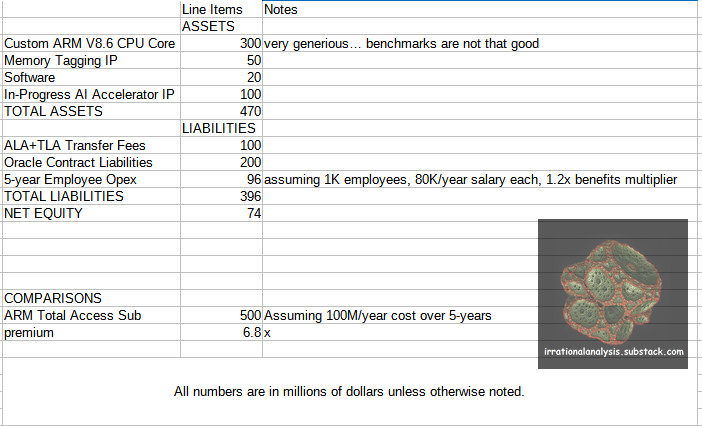

[4.a] Assets

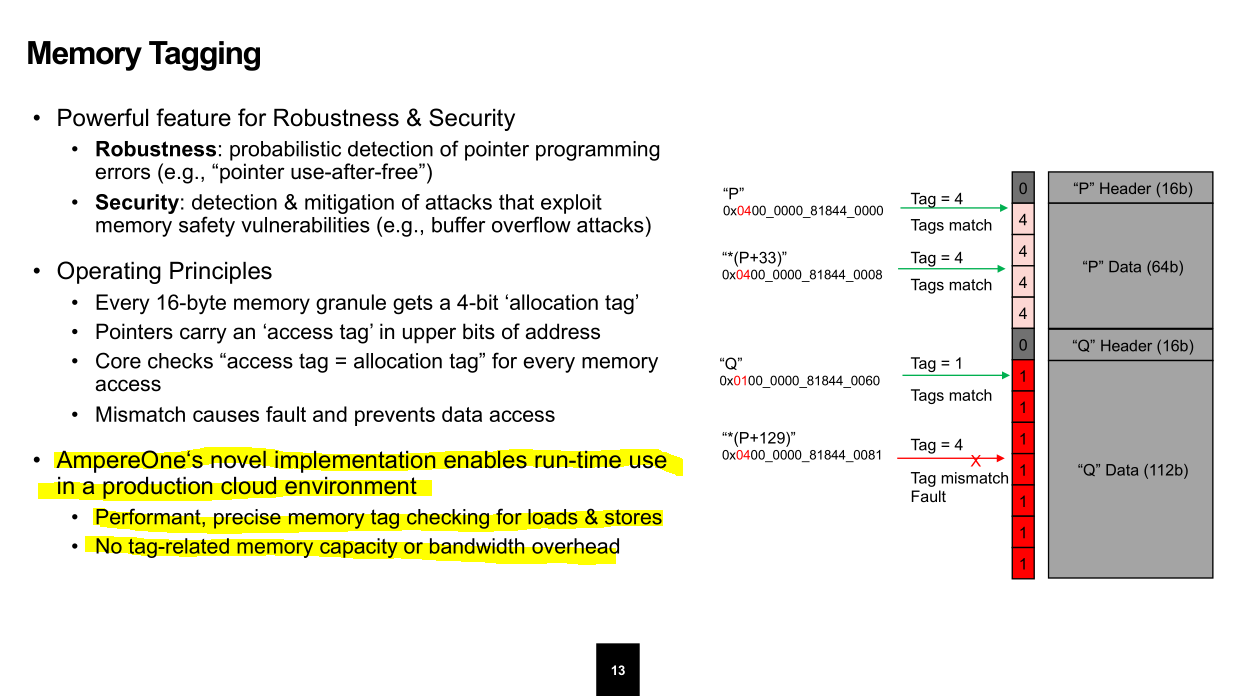

A prospective buyer would gain access to Ampere Computing’s custom ARM V8.6 CPU core IP, a software stack that has some value over open-source ARM tools, and a handful of custom bells and whistles such as their unique memory tagging implementation.

Memory tagging in runtime usually kills performance. They claim this implementation has such a negligible performance impact, it can be used in production by default.

[4.b] Liabilities

Ampere Computing is rumored to have over 1,500 employees globally. This is comically bloated given the size and projections of their shrinking business. I will assume that the buyer will cut 30% right out of the gate and guess payroll+benifits liabilities of the remaining 1,000 employees.

Contracts with Oracle for pre-paid chips and mandatory support of old chips until 2030 also count as significant liabilities.

Finally, the ALA with ARM (the corporation) has to be viewed as a liability, not an asset. The Qualcomm/Nuvia lawsuit clearly states that ARM management and legal do not believe ALAs are transferable from an acquisition.

If any prospective buyers think that they can acquire Ampere Computing and get some cheap ARM licenses, think again.

[4.c] Rough Valuation Framework: VS ARM Total Access

The best comparison I can think of is buying Ampere Computing vs. paying for an ARM Total Access annual subscription.

Here is a very rough valuation framework I have cobbled together. My background is engineering, not finance so don’t take this too seriously.

I believe Ampere Computing is worth $75M.

Ampere Computing is a deeply impaired asset and should be valued as such.

Now how much is Intel worth :p

What's the argument against using Ampere's cloud cpus? I know the hyperscalers are building their own (graviton, etc.) but there still seems to be signifigant appetite for Intel's new e-core based chips (sierra forest, clearwater forest). Is it just that the clouds still want some x86 capacity, but for ARM workloads they are better off with their own chips?

I'm not sure how big the business is for non-hyperscaler deployments (like in a supermicro or dell server rack for smaller deployments).