2023 End-of-Year Portfolio Update

IMPORTANT:

Irrational Analysis is heavily invested in the semiconductor industry.

Please check the ‘about’ page for a list of active positions.

Positions will change over time and are regularly updated.

Opinions are authors own and do not represent past, present, and/or future employers.

All content published on this newsletter is based on public information and independent research conducted since 2011.

This newsletter is not financial advice and readers should always do their own research before investing in any security.

DO NOT SHARE INSIDER INFORMATION OF ANY KIND IN THE COMMENTS SECTION. (Leaked info or rumors from **other** corners of the internet is ok)

Hello wonderful subscribers. Happy new year!

To celebrate the last trading day of 2023, I want to share a more detailed view of my holdings and investment plans for 2024.

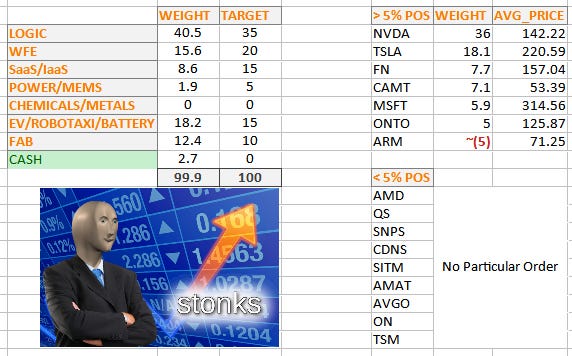

Portfolio: 2023 Edition

Any position that is > 5% of NAV gets average price and overall % of portfolio disclosed. Smaller positions are lumped up into sector categories.

*Note: Broadcom is split 50% LOGIC // 50% SaaS/IaaS.

**I have no other liabilities other than the ARM 0.00%↑ short.

2024 Plans:

Reminder that this is how I plan to invest my own money.

NOT INVESTMENT ADVICE

DO YOUR OWN RESEARCH

Buy:

MSFT 0.00%↑ SNPS 0.00%↑ CDNS 0.00%↑ AVGO 0.00%↑ CAMT 0.00%↑ ONTO 0.00%↑ AMAT 0.00%↑ FN 0.00%↑

Microsoft:

Excellent, smart, competent CEO.

Azure » AWS »»»» Google Cloud

Enterprise SaaS (Office, Teams, SharePoint, …) is sticky, macro resistant, and growing.

I like Arkane Studios, owned by Bethesda, owned by Microsoft.

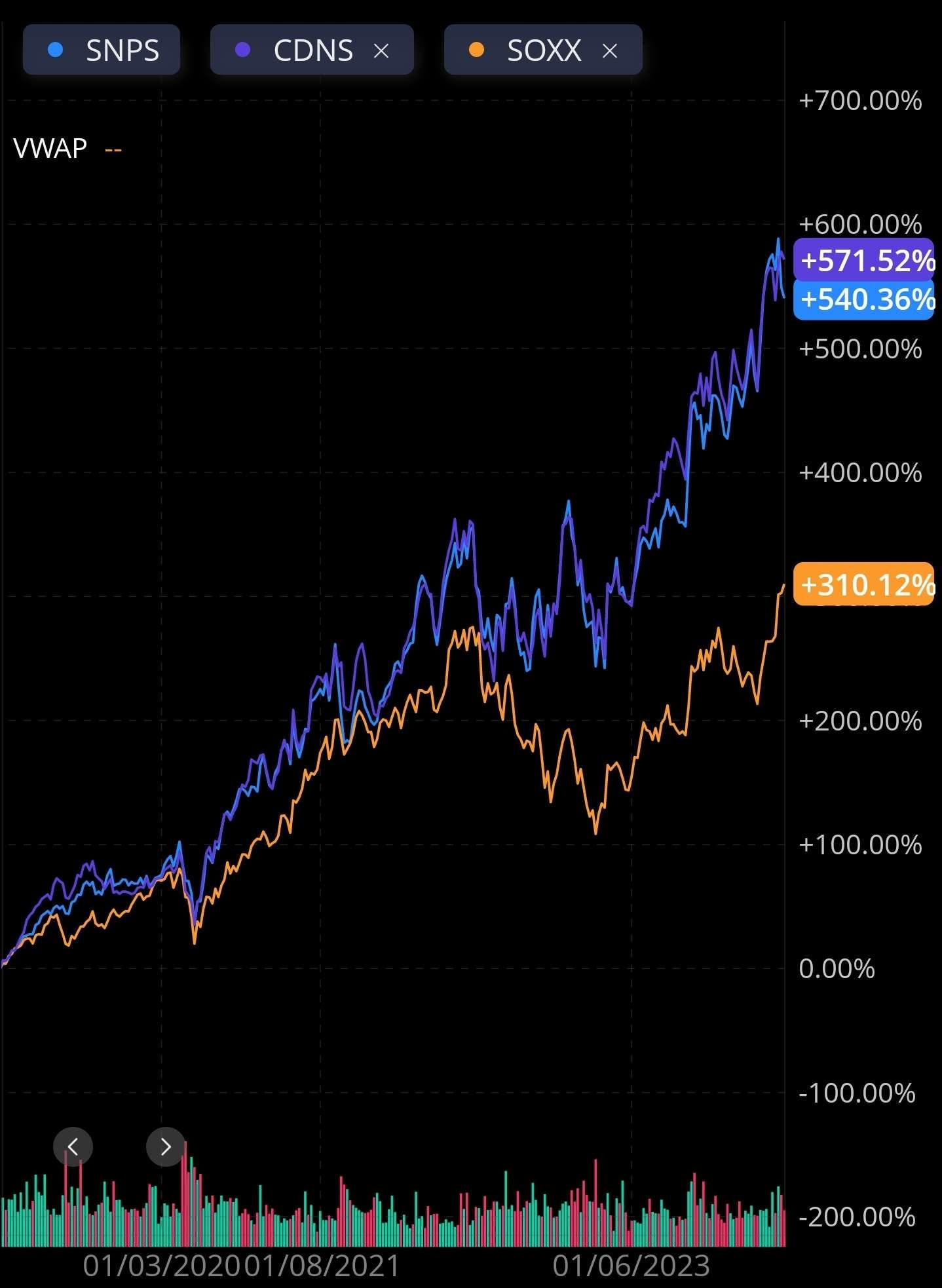

EDA (Synopsys/Cadence):

Complexity is growing so they are charging more for new features, particularly AI-enhanced optimization tools.

More companies are designing their own chips, leading to structural growth.

Safe, sticky SaaS business.

Synopsys buying Ansys is smart. Good strategic move.

Look at this chart… see the outperformance relative to SOXX?

Broadcom:

With VMWare closed, revenue is half semi and half SaaS so buying shares is diversification neutral.

VMWare’s comically bloated middle management has been eviscerated. (Hock Tan did not need to cut 50%… he could have cut 35-40% and allowed the remaining employees to suffer less but oh well…)

Google TPU ramp.

Excellent networking products. (Tied with Nvidia/Mellanox IMO)

CamTek/Onto:

Interested in advanced packaging metrology.

Each has its own risks:

CamTek factory might get blown up by Hamas missile and/or other war/geopolitical problems.

Onto has memory exposure and I hate memory market.

Applied Materials:

Good overall business. (diversified, dividend, stable, good products)

Sculpta stool is awesome and market has not priced it in properly IMO.

Sculpta is also a way of leveraging towards Intel Foundry growth without owning Intel shares. (most of my portfolio is busy devouring Intel design groups market share)

Fabrinet:

Optics is the future.

Nvidia bailed them out from a disastrous Teleco cycle.

Solid overall business.

ON Semi:

Silicon carbide.

Power electronics diversification.

Watch:

SITM 0.00%↑ SMCI 0.00%↑ AEHR 0.00%↑ ALB 0.00%↑ BHP 0.00%↑ INTC 0.00%↑ QS 0.00%↑ ENTG 0.00%↑

These are stocks that I might buy in 2024 depending on news.

I have small SiTime and QuantumScape positions and don’t feel the need to accumulate.

AHER, ON, Albemarle, and BHP are getting hit hard by EV recession and China macro.

Super Micro is a little sus and risky. Not comfortable touching this one but it is very interesting to watch.

Intel shares are toxic until the inevitable design/foundry split happens.

Trade:

AMD 0.00%↑ QCOM 0.00%↑ ARM 0.00%↑

AMD used to be my largest position. Sold out most of it this year to diversify and because of Nvidia crazy AI ramp devouring datacenter CapEx. Still own some shares because Xilinx/FPGA and datacenter CPU (EPYC) are very good.

MI300X is ok and only viable for single-node inference until Q3 2024 before Nvidia closes their window.

Because of a disconnect between narrative and engineering reality, I have been trading covered AMD calls on margin (20-25% NAV) and will continue to do so.

Qualcomm and ARM are both tied to the smartphone market. Apple and Huawei are making big moves and China macro is causing a lot of chaos.

I believe ARM is comically overvalued. Opened a short position at 5% of NAV. Might increase it next year.

Qualcomm is hemorrhaging share to MediaTek, Apple, and Huawei with tiny diversification outside of smartphone.

CEO has no vision. “Connected Intelligent Edge” means “desperately try to generate accretive margins on modem technology”, which is rapidly being commoditized by MediaTek, Apple, and Huawei. Even in an optimistic scenario where automotive revenue ramps to 1B/quarter (100% YoY growth… not happening) and laptop/PC share goes from < 0.1% (yes it really is that bad) to ~2% (20x YoY because Elite X is very good but launches in H2), they still will miss sell-side estimates by a wide margin in 2024.

The recent rally is primarily because sell-side was expecting 20-40% share with Samsung for the 2024 Galaxy series and Qualcomm apparently got 80%. (Hint: It is because S.LSI botched something.)

QCOM seems like a fun options trading opportunity. Their CFO is rather predictable and likes to technically meet guidance for current quarter but massive guide down.

Degenerate gambler me is going to try and play earnings weeklies throughout 2024.

Remember…

“It’s just money. It’s made up.” — John Tuld