MaxLinear Implosion, Apple Modem

MaxLinear Implosion, Apple Modem

$MXL crashes and burns. $QCOM is out of runway.

IMPORTANT:

Irrational Analysis is heavily invested in the semiconductor industry.

Please check the ‘about’ page for a list of active positions.

Positions will change over time and are regularly updated.

Opinions are authors own and do not represent past, present, and/or future employers.

All content published on this newsletter is based on public information and independent research conducted since 2011.

This newsletter is not financial advice and readers should always do their own research before investing in any security.

If you have a lot of semiconductor investments (like me), today was a bad day.

MXL 0.00%↑ had a much worse day because of disastrous earnings.

MaxLinear forecast revenue for the third quarter of about $70 million to $90 million.

THIRD QUARTER FORECAST

Sees revenue about $70 million to $90 million, estimate $111.2 million (Bloomberg Consensus)

Sees adjusted gross margin 57% to 60%, estimate 60.2%

SECOND QUARTER RESULTS

Net revenue $92.0 million, -50% y/y, estimate $100 million

Adjusted gross margin 60.2% vs. 61% y/y, estimate 60%

Adj. R&D expense $48.2 million, -16% y/y, estimate $49.2 million

Adjusted operating margin -21% vs. 16.2% y/y, estimate -14.8%

Adjusted loss per share 25c vs. EPS 34c y/y, estimate loss/shr 19c

Negative cash flow from operations $2.70 million vs. positive $30.6 million y/y, estimate negative $14 million

MaxLinear is a company with two major business segments:

New PAM4 optics DSP for AI networking.

Built on Samsung 4nm-class process node.

Competes with MRVL 0.00%↑ (80% share) and AVGO 0.00%↑ (20% share).

Probably garbage but it will be dirt cheap, go from 0% market share to something, and is a massive TAM.

A variety of wireless, telco, WiFi, DOCSIS garbage.

Instead of saying “net loss from operations” they said, “cash used in operations”. LOL

I am 99.9% confident the US government revoked MaxLinear’s license to sell to Huawei was revoked. MXL 0.00%↑ probably was selling to some middle-man or shell company who was then re-selling to Huawei, who has now been blacklisted.

Here is a quick explanation of what “wireless infrastructure” means for MaxLinear.

The red circles are microwave and mmWave backhaul antennas. This is not the same mmWave your 5G smartphone connects to.

Carriers need to link up many cell towers to a core network which then goes to internet infrastructure. This means fiber. Expensive fiber.

One common way to get around this fiber problem is by connecting towers together with dedicated wireless backhaul. If you ever happen to go near a cell tower side and see a warning…

It is because of this wireless backhaul antennas. Massive power blasted at line-of-sight to neighboring cell towers. The FCC takes safety very seriously. Rules and regulations around RF exposure to people are very strict.

Anyway, MXL 0.00%↑ makes a ton of components related to this backhaul stuff. Telco CapEx is already shit. What little spending there is goes to digital infrastructure upgrades, not backhaul.

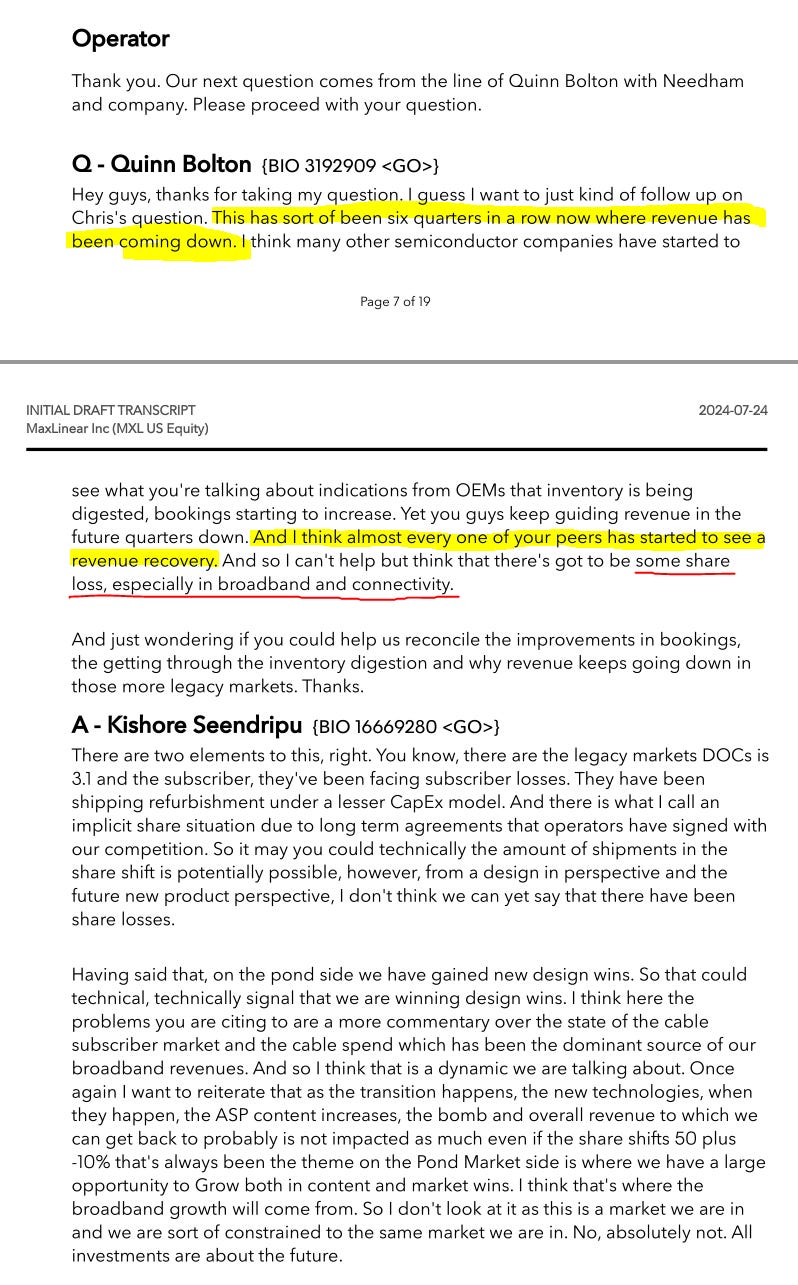

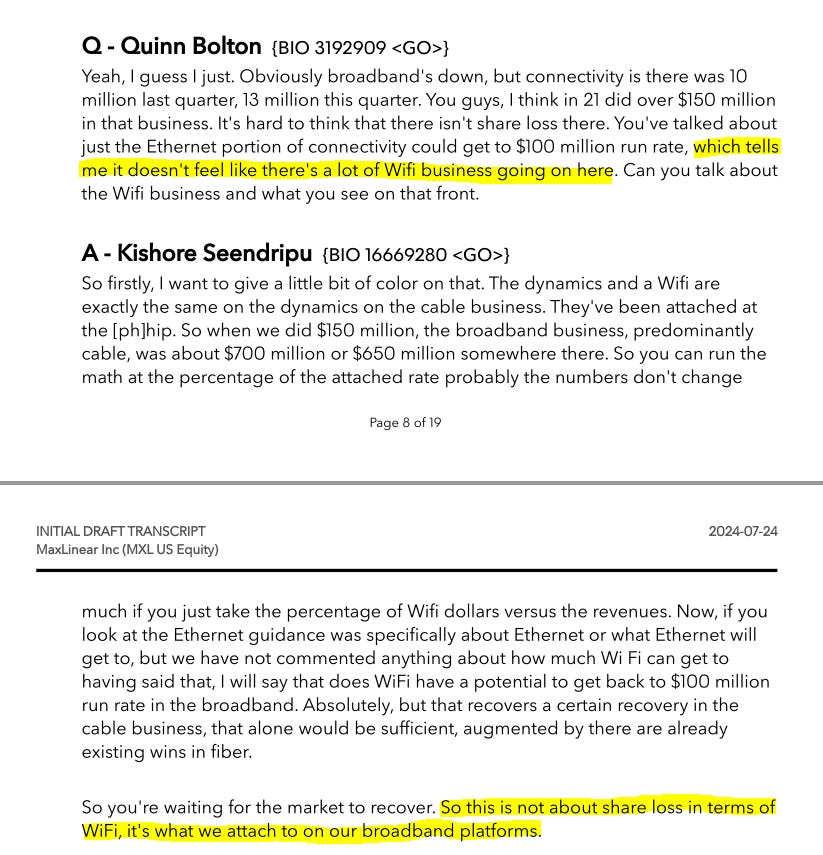

Needham analyst has a point. The only logical explanation for this disastrous print is that MaxLinear is hemorrhaging share in DOCSIS, WiFi, PON, and other broadband/connectivity markets.

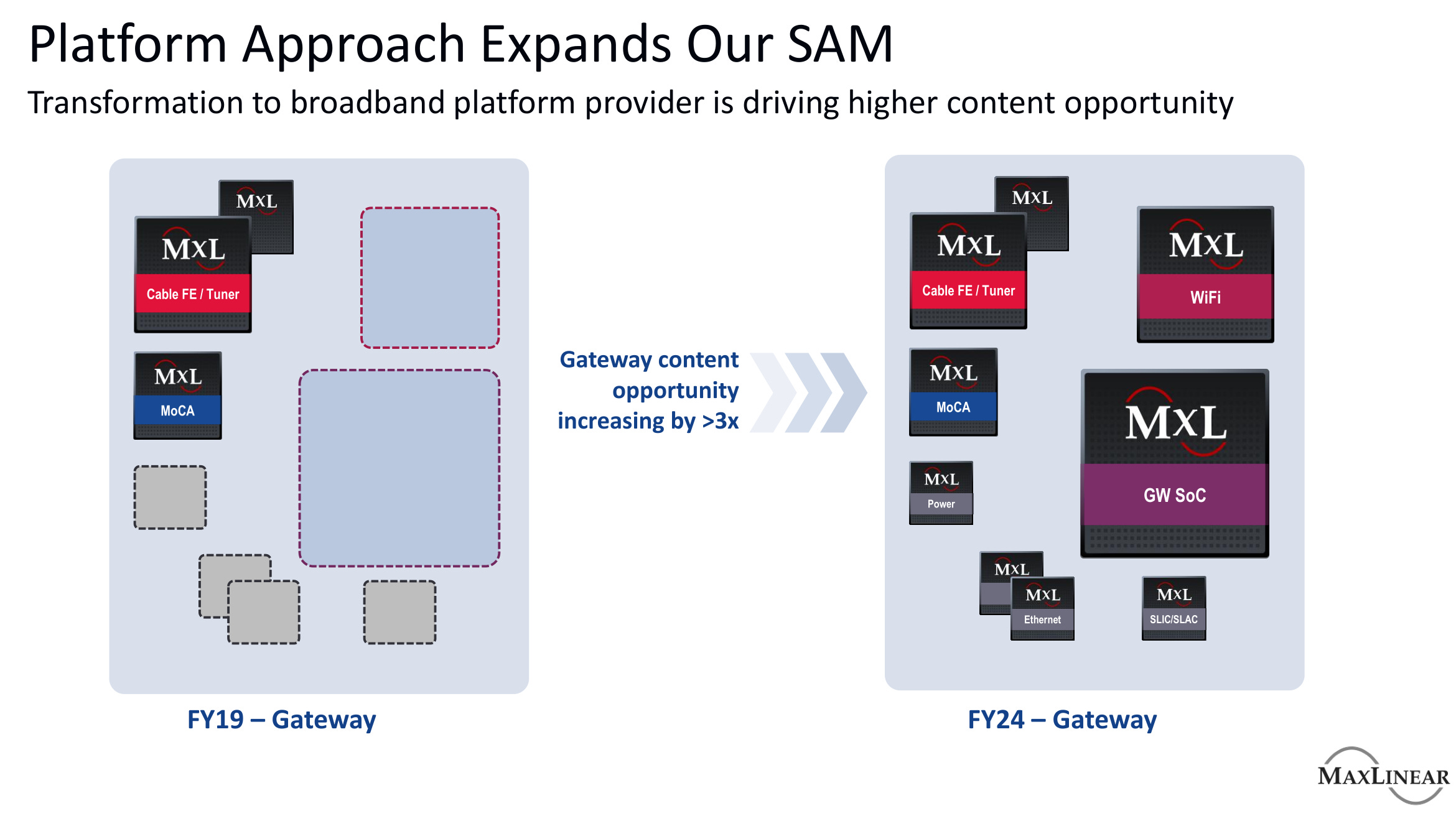

MaxLinear bought Intel’s gateway unit for dirt cheap some time back and has enjoyed nice bundling opportunities as highlighted in their overview slides.

The problem is… AVGO 0.00%↑ and MediaTek ($2454.TW) can bundle a complete solution too. MaxLinear appears to be getting squeezed on both quality (high-end Broadcom solution) and price (low-end MediaTek solution), hemorrhaging share in the process.

Needham analyst is very clever. Goes in for the kill.

We are not losing share in the WiFi market, we merely failed to attach our WiFi to our broadband platforms. 🤡

THIS IS SHARE LOSSES. CORPO BULLSHIT SPEAK.

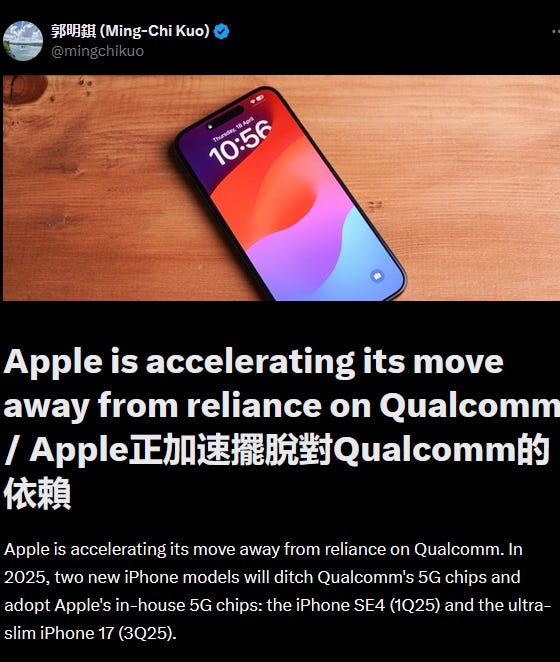

Now on to the other big news of the day within wireless.

I am extremely surprised by this news. Ming-Chi is one of the best analysts for mobile and Apple supply-chain in particular. He is legit. This news is legit.

My previous base case was Apple using their own modem in the 2026 SE iPhone with full line-up conversion in 2027.

So QCOM 0.00%↑ gets 100% share in 2025, 80% in 2026, <10% share in 2027 (Q1 shipments before patent license expires), and 0% share afterwards.

Apple has apparently gotten their modem working much earlier than expected. Looks like QCOM 0.00%↑ only gets 40-50% share in 2025 and less than 20% in 2026.

This is disastrous. All the incremental revenue from the growing/good business units at Qualcomm (Auto, Laptop/PC) will get wiped out several times over by the hole Apple is about to punch through Qualcomm’s financials.

I have initiated a large short position against QCOM 0.00%↑ based on this news. Also have a large short position recently opened against AMD 0.00%↑. Parked some of the cash in AVGO 0.00%↑ and holding on the rest for dip-buying in names I like.

All semiconductor names have been hit hard with somewhat equal pain. It’s time to pick winners and losers…. with leverage.

Bear:

Bull:

By end of year, I am going to crush the index by which I benchmark myself against, SMH 0.00%↑, or blow up my primary account while trying.

It’s just money. It’s made up.

YOUR WRITING IS JUST AMAZING🫡

I’m curious, what’s your bear case for AMD? A resurgent INTC? Not being able to do much in AI/GPUs? ARM server CPU competition whether cloud optimized or not? ARM client CPUs?