[4QCY24] Marvell, Broadcom, Micron

Two AI winners and a hilarious loser.

Irrational Analysis is heavily invested in the semiconductor industry.

Please check the ‘about’ page for a list of active positions.

Positions will change over time and are regularly updated.

Opinions are authors own and do not represent past, present, and/or future employers.

All content published on this newsletter is based on public information and independent research conducted since 2011.

This newsletter is not financial advice, and readers should always do their own research before investing in any security.

Feel free to contact me via email at: irrational_analysis@proton.me

Welcome to a special earnings roundup. Managed to make a good amount of money on all three prints.

Things are a bit chaotic now because Lord Powell said naughty things (no presents for you!) and I am scrambling to de-lever and withdraw money to pre-pay capital gains taxes.

There will be a full portfolio update on December 31st followed by a special “irrational/contrarian/dangerous” ideas research report on January 1st.

In the interest of transparency, here is my YTD P&L for MRVL 0.00%↑, MU 0.00%↑, and AVGO 0.00%↑.

Very brief opinions on these three:

Broadcom is an excellent long-term investment. Buy and hold for many years. Look at my post history. Been very consistent and detailed on this.

I maintain a very large, long position via shares (#2 position behind Nvidia) and have no intention of selling.

Marvell is toxic to me right now. Want nothing to do with this stock. More on this in the Jan 1st post.

Currently hold no position and no intention to touch this.

Micron is very interesting now that it shit itself. I have a very non-consensus thesis. Again, gotta wait until Jan 1st.

Currently hold no position but browsing the options chain like a salivating degen gambler.

Now let’s go over the earnings calls.

Micron:

By far the most entertaining earnings call. Prepare yourself for some legendary copium.

MICRON SEES 2Q ADJ. REV. $7.7B TO $8.1B, EST. $8.99B 💀

MICRON SEES 2Q ADJ GROSS MARGIN 37.5% TO 39.5%, EST. 41.3% 💀

This is a faceplant.

There is no AI PC refresh cycle. This was an obvious, delusional hopium narrative from the start.

24 GB of DRAM on laptops? LAMO

Windows 10 EOL wont save you. My employer literally upgraded all the (rather old) employee laptops to Win 11 earlier this year.

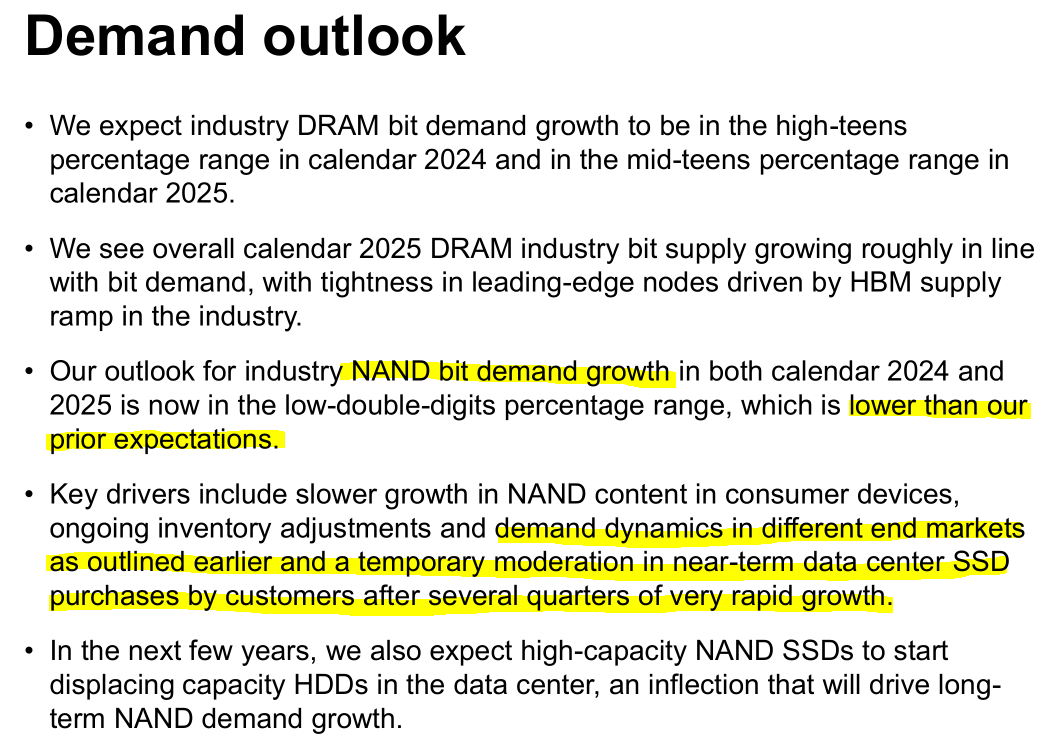

YMTC…? Is that you destroying the NAND market?

YMTC and CXMT are about to have a lot of fun.

They are giving up NAND share to YMTC.

“Customer inventory” comments are usually bullshit. They are losing share to CXMT and YMTC.

Datacenter SSD lumpiness is fine. Legit excuse.

HBM3e ramp is later than expected.

YMTC NAND is going to crush Micron’s gross margins for another two quarters at minimum. This headwind overpowers gross margin accretion from HBM. lol

The bull case for Micron is they gain share from Samsung. Not just via units/bits but via ASP and gross profit as well.

I have a lot of thoughts on this. Jan 1st gona be hype.

Micron CEO dodged the question. It is very important to think about why they hiked TAM despite fixed prices in the contracts signed with Nvidia. Yield improving rapidly would be a neat explanation to the cryptic messaging by Micron.

One of the bull cases for Micron was that HBM wafer intensity is ~3x of normal DRAM. This would cause regular DRAM prices to spike due to supply destruction/cannibalization. Unfortunately for them, CXMT is ramping DDR5+LPDDR5 right now at excellent 80% yield.

Buddy. It’s only Nvidia GB systems. Nobody else bothers with trash LPDDR5 in their system.

CXMT is not a “18-24 month” in the future problem. They are ramping DDR5 and LPDDR5 right now at 80% yield!

Micron CEO basically went :seenoevil: and tried to pretend that there is no threat.

Haha PRC is only competing in the low-end which is 10% of our revenue. Everything is fine haha.

Broadcom:

Hock Tan says some hyper-bullish things that caused the stock to spike. Crazy stuff. I had call options up 150% and paper-hands sold before earnings. Could have been up way more.

The three hyperscale customers are Google, Meta, and Bytedance.

The two new hyperscale customers are OpenAI and Apple.

LOOOOOOOL

Marvell:

There are rumors that Trainum 3 has been moved (partially or completely) to Alchip.

Way too many people have pinged me on this. Jan 1st post will include an attempt to parse the rumors.

There are rumors the Microsoft Maia 2 ramp is going to be bigger than Amazon/Trainium and Google/Axion combined.

Thank you for the roundup!

You are so good!! 🔥🔥

I guess now I’ll start DCAing into SiTime. Waited to long to pull the trigger and now it’s much higher (probably should have bought when fabricated knowledge talked about them https://www.fabricatedknowledge.com/p/its-high-time-to-look-at-sitime). I still think their technology is really interesting though I don’t know too much if they have a moat.